Interesante lo que ha ido comentando Altria en estos resultados. Comento algunas cosas que, de primeras, me han parecido interesantes.

Juul

Juul had net revenues in excess of $1 billion in 2018, up from approximately $200 million in 2017. Juul overwhelmingly reaccelerated the U.S. e-vapor category growth rate growing Juul’s volume by nearly 600% to over $450 million, refill kit pods. We estimate Juul represents over 30% of the overall e-vapor category across open and closed systems, and all-trade classes. After e-vapor growth plateaued from 2015 to 2017, rapid growth was reignited in 2018. And we expect U.S. e-vapor volume to grow at a compounded annual rate of 15% to 20% through 2023.

As a reminder, Altria share of Juul’s international e-vapor income would be 100% incremental to Altria. We believe the global e-vapor and heat-not-burned segments with estimated sales of roughly $23 billion in 2018 have substantial room to grow. Juul currently operates in eight countries with plans for additional expansion this year. We expect the Juul product features that have driven Juul’s success in switching adult smokers in the U.S. to strongly appeal to international adult cigarette smokers. And Juul has designed products [ph] in international markets to meet applicable regulatory requirements and also has significant new innovations in its pipeline.

Let’s look at two examples. First, in Canada, where distribution is limited, Juul reports that retail takeaway grew to more than 60% dollar share in stores selling their products after only three months at retail. Juul is also seeing encouraging performance where they have achieved distribution in Europe. For example, in the Sainsbury Chain in the UK, Juul tells us that it recently became the number one e-vapor brand in the chain with a dollar share in excess of 23% in less than 12 weeks after launch. And just to remind you, the UK operates under the tobacco products directive adopted by many EU countries, which limits the nicotine concentration level. Ultimately, we expect the international revenue and income opportunity to end up being as large as or larger than the U.S. opportunity. Our 35% investment was based on a deep strategic operational and financial analysis of Juul in the marketplace.

Clearly, we look at this opportunity over the long term, but for context, let us provide a view of five years out. Some of our independently developed key assumptions over the next five years that informed that analysis include a U.S. e-vapor category with a gross volume between 15% to 20% annually. Juul continuing to be the primary growth driver for the e-vapor category. Attractive Juul operating margins that achieved current cigarette-like-margins due to the benefits of increasing scale and automation in the supply chain. International revenues that equal domestic revenues by 2023 and international margins that approach current international cigarette margins.

Under our assumptions, our investment in Juul would generate an after-tax return exceeding our weighted average cost of capital in 2023. Additionally, with five year e-vapor category volume growth in the range of 15% to 20% annually, we would expect the U.S. cigarette category volume decline rate to be consistent with the decline rate estimate of 4% to 5%. I’ll remind you that in 2018 with e-vapor category volume growth of 35%, the cigarette category decline rate was 4.5%, including a 0.5% headwind from gas prices. Combined with the earnings and cash generation engine of our core tobacco business, we believe this investment in Juul will support consistent returns over the long-term by providing Altria with a significant stake in the fastest growing – in the fast growing e-vapor category.

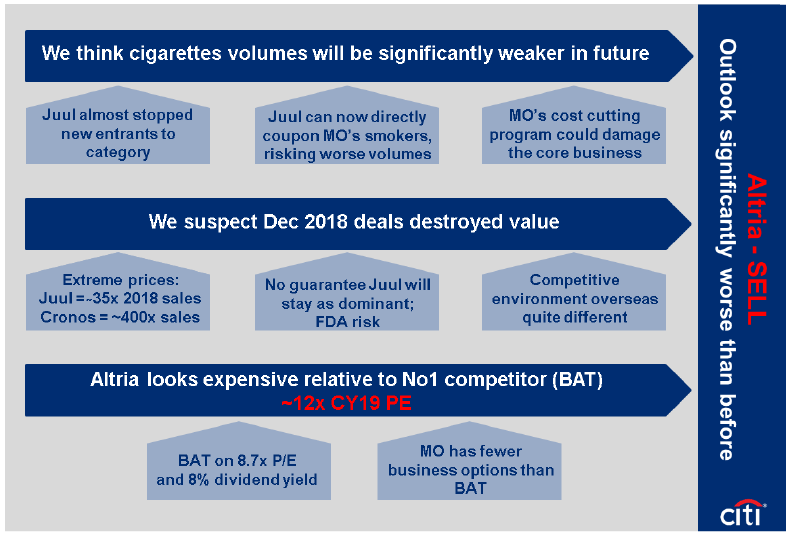

La verdad es que pocas startups han salido como esta. Y… con la distribución de la mano de Altria cada vez me parece menos descabellada la inversión. Parece ser que,como apunta @madtrad, fuera de USA también lo está haciendo muy bien (esto es muy interesante para MO). Sigo manteniendo mi postura: inversión difícil de cuantificar en estos momentos y solo el tiempo dirá si ha sido un regalo o un bluff.

Cronos

Let’s now turn to Cronos. While the transaction is subject to customary closing conditions and expected to close in the first half of 2019, Altria’s agreement to acquire a 45% stake in Cronos with a warrant to achieve majority ownership will create a new growth opportunity in an adjacent category poised for rapid growth. It complements our strong core tobacco businesses and expands our income opportunity beyond the U.S. After years of evaluating adjacent opportunities the cannabis category is quite attractive and delivers on some key considerations including accretion to our long-term financial performance and synergy without Korea’s [ph] capabilities, allowing our combined resources to accelerate Cronos growth. While a range of estimates exist, a recent third-party report projects the 10-year global cannabis revenue opportunity to be in a range of $40 billion under a similar legal landscape to today to more than $250 billion assuming a fully legal market worldwide.

Pues un poco en la linea de Juul en lo que se refiere a buscar expansión internacional (MO no vende tabaco fuera de USA). Y lo que todos sabemos: un mercado potencialmente enorme que guarda sinergias con el negocio del tabaco y de los nuevos dispositivos. Mi duda siempre ha sido si la maría es un producto commodity (similar a lo que sería la lechuga) o si por el contrario se puede diferenciar y crear marca. A raíz de comentarios como los de @angelitoo y de @enginvert estoy mas en este segundo punto.

Parece que van a usar la cantidad de dinero que sobra del crédito para comprar Juul, para aumentar la participación en Cronos.

Iqqos

Harm reduction remains central to our view of the future for the tobacco industry. In addition to the significant opportunity presented by e-vapor, we remain very excited about the prospects for heat-not-burned in the U.S. It is now approaching two years since PMI submitted the IQOS PMTA and we are fully prepared to commercialize IQOS in the U.S. We remain fully committed to the success of IQOS in the U.S. and are excited to deploy our robust commercialization plans. PM USA is establishing brick and mortar stores, including locations in multiple cities within the first year of launch. They’ve already hired personnel to support prelaunch activities and are collaborating with key partners to best position IQOS at retail.

Parece que este año si que van a empezar a comercializarlo. Veremos como va.

Resultados.

En cuanto a lo que es el guidance de la compañía. Básicamente crecimientos de EPS 4% to 7%. Casi me parece milagroso y no demasiado lejano a lo que uno podría esperar de una compañía como MO (incluso en un momento más estable). Máxime teniendo en cuenta:

- El aumento de los costes finacieros por la deuda para las compras.

- Los costes que implicará el lanzar Iqqos al mercado.

- El recorte del dividendo de BUD (que además yo creo totalmente necesario).

- La canibalización que suponen los nuevos productos.

En fin, que parece razonable esperar tranquilamente cobrando el dividendo (que al menos con este guidance paree a salvo) mientras uno espera a que florezcan las inversiones (si es que lo hacen) y se estabilice un poco la cosa en BUD.

Esto no es ninguna recomendación de comprar, la compañía, como todas, tiene sus riesgos y además, en mi opinión, todos estos cambios tardarán en ir dando sus posibles frutos.