Nuevo análisis de PM en M*

PMI Backing the Right Horse, but Perpetual Investment May be Required to Drive iQOS

Business Strategy and Outlook | by Philip Gorham Updated Mar 12, 2019

After a promising start, the adoption of iQOS, Philip Morris’ heated tobacco platform, slowed materially last year, and investors are now questioning the future of the category. The slowdown should not be surprising, however, as history shows the diffusion of disruptive consumer products has rarely occurred in a straight line, with various consumer segments adopting new products at different rates. With the adoption of the first platform having plateaued at fairly low levels, however, we think more disruptive innovation is required if heated tobacco is to mitigate the impact off the decline in combustible volumes.

Of all the e-cigarette incarnations, heated tobacco products most closely replicate the smoking experience and so should attract smokers looking for a less risky alternative, so we believe that Philip Morris’ multiple premium over peers is appropriate because it has claimed a first mover advantage, at least temporarily, through the early commercialization of iQOS. However, there are still many unanswered questions about the evolution of heated tobacco. Much depends on the regulatory environment, and whether regulators publicly acknowledge that the category is safer than smoking. The FDA is expected to announce its opinion later in 2019. Margins are also a key concern. We think that with scale, heatsticks can be at least as profitable as premium cigarettes, but margins will depend heavily on the level of taxation, and our base case assumption is that heatsticks are taxed in most markets as tobacco products.

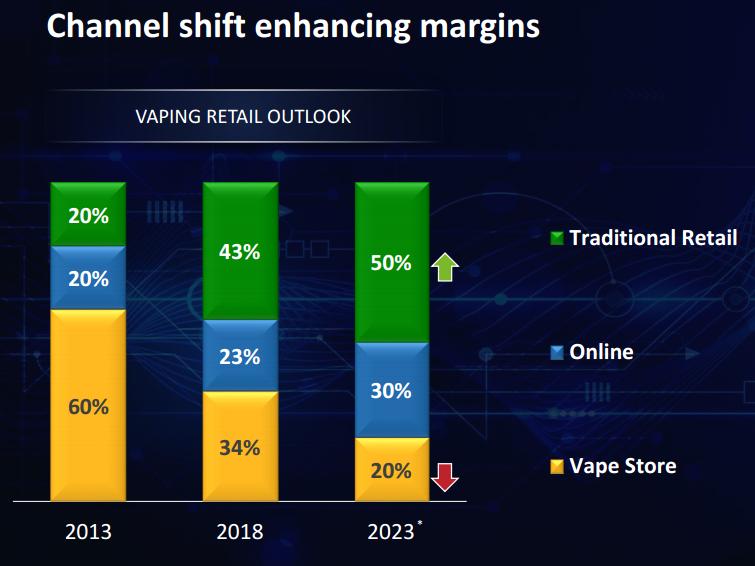

One drag on category profitability is the low margins on devices. We estimate iQOS devices generate margins of approximately 10% at full price and breakeven when on discount. It does seem likely that devices will never be as high margin as the stocks, given the likelihood of the development of a razor-and-blade model, but pipeline products such as PMI’s platform 2, the disposable heated tobacco stick branded as TEEPS, has the potential not only to avoid this profitability impediment, but also to reignite growth in a category that has caused both euphoria and disappointment amongst investors.

Economic Moat | by Philip Gorham Updated Mar 12, 2019

Philip Morris International possesses a formidable franchise in the tobacco industry, formed by the aggregation of intangible assets and a cost advantage. Tight government regulations have made barriers to entry almost insurmountable and have kept market shares stable. Consumers are quite brand-loyal, particularly in premium price segments, to which PMI’s portfolio skews, creating another intangible asset that is no longer as prevalent as it once was in other consumer categories. Finally, economies of scale give the large-cap manufacturers an advantage in tobacco leaf procurement and distribution.

Intangible Assets

Tobacco contains nicotine, an addictive substance that suppresses the cessation rate. According to data from the Tobacco Atlas, more than 60% of all smokers intend to quit, and 42% have attempted to quit over the last 12 months. Yet in most markets, the smoking rate is in only a very modest decline, implying that the majority of smokers attempting to quit fail to do so. Academic research (Lewis and others, 2015) has shown that while cessation rates are not correlated with consumer brand loyalty, premium price segments are associated at a statistically significant level with lower cessation rates. According to company disclosures, PMI has the heaviest skew to premium segment among the large-cap cigarette manufacturers, with around 55% of its OECD volumes in premium segments, benchmarked against roughly 25% for the industry in aggregate. PMI’s leading premium brands are Marlboro and Parliament.

The addictive nature of the product forms a powerful competitive advantage when combined with very tight government regulation that over the years has dampened market share volatility and competition on price. Tobacco advertising is severely restricted in most markets, with bans on most forms of mass marketing. This not only makes it very difficult for hypothetical new entrants to gain the attention of smokers, but it also dampens competition between incumbent manufacturers. Volume shares at the manufacturer level have been very stable for decades, primarily, we believe, because the lack of marketing communication has discouraged brand switching. PMI has been the only cigarette maker to increase its market share organically–by just 30 basis points–on a global basis excluding China since 2008. Marketing spending intensity varies across consumer product categories, but on average, manufacturers in more competitive categories roughly spend a high-single-digit percentage of sales on marketing. Big Tobacco manufacturers have historically spent around 1.5% of sales on advertising (although we expect next-generation products to require greater spending), with the difference accruing to the EBIT margin. Some other regulations may also have had the unintended consequence of limiting competition on price and creating a barrier to entry. Point-of-sale display bans limit manufacturers’ ability to communicate pricing, thus creating a disincentive to engage in price promotional strategies, which have historically contracted the industry profit pool. PMI makes no sales in the U.S., but FDA oversight of the U.S. has created perhaps the most clear-cut example of regulation creating insurmountable barriers to entry. The marketing of new tobacco products is subject to FDA approval, which is only granted following consideration of a request to market a new product (PMI’s ongoing application to market iQOS as a modified-risk tobacco product) or for requests made before March 2011, under the substantial equivalence test, which limits marketing approval only to products that are proven to possess similar characteristics and risk profiles to predicate products.

Despite consumer segmentation in other consumer product categories amid eroding brand loyalty, brand equity remains relevant in tobacco. This is in no small part due to the absence of challenger brands because of high regulatory barriers to entry, and because of the tight restrictions on marketing. Brand loyalty tends to be higher in premium price segments, which benefits PMI disproportionately.

Cost Advantage

Cigarette manufacturing is a scalable business model because of the homogeneity of the product, and there is an inverse correlation between volume and average operating cost per unit. In 2018, we estimate that PMI’s operating costs per pack of cigarettes and Heatsticks (after adjusting for devices) was $0.45 on volumes of 782 billion sticks. At a cable rate of 1.30, we estimate comparable costs per pack were $0.63 for Imperial Brands (in the fiscal year to Sept. 30, 2018), on less than half the volume of PMI, and $1.10 for Altria, after adjusting for the MSA payments, on volumes of just 14% that of PMI. The difference in the cost structure lies primarily at the gross margin, implying procurement advantages from scale.

Wide Versus Narrow

Though it may seem counterintuitive in a declining industry, we have conviction that our wide moat rating is appropriate because we believe PMI is very likely to continue generating excess returns on invested capital for the next 20 years. The sustainability of current levels of profitability and returns on capital depend on the positive impact of price/mix being at least in line with the annual volume decline. At some point in the future, we anticipate a tipping point at which the consumer is no longer willing to continue to accept price increases above the broader rate of inflation, leading to an increase in price elasticity. The example of Australia gives some insight into how such a kink in the demand curve might occur globally. Since 2011, a series of Draconian anti-cigarette measures in Australia have led to the introduction of plain packs and a tax increases that caused the doubling of the retail price of cigarettes in just six years, which in turn has led to the smoking rate falling from 16% to 13% over the same period, and to significant trading down between price segments. A pack of 20 cigarettes (equivalent; a standard pack contains 25 sticks in Australia) now costs roughly USD 14.50, well above the USD 10.40 average retail price in the U.K., USD 5.50 in the U.S., and USD 4.87 on average globally, according to the World Health Organization. Assuming the Australia experience is applicable to price elasticity in other markets, it appears likely that there remains a great deal of headroom for price increases globally. At 4% real pricing (based on the 6% nominal price/mix PMI has achieved over the past three years and 2% global inflation), this crude calculation suggests that it will be 2046 before global pricing reaches levels at which price elasticity increased in Australia. This is comfortably longer than 20 years, the benchmark period that we expect wide-moat companies to continue generating economic rent.

Fair Value and Profit Drivers | by Philip Gorham Updated Mar 12, 2019

Our fair value estimate is $102, which implies forward 2020 multiples of 18 times earnings per share, 13.7 times EV/EBITDA, a free cash flow yield of 5%, and a dividend yield of 5%. These implied multiples are at the high end of both the historical trading range of the tobacco industry and our valuation of the tobacco group; we think this is justified by PMI’s advanced position in heated tobacco, which we believe has the potential to slow the industry consumption decline rate.

The overarching assumption relating to reduced-risk products in our base-case valuation is that iQOS continues to increase its share of PMI’s volume mix and that this is margin dilutive. We assume a midcycle margin of 39.7%, slightly above the 38.5% achieved last year, when currency was a headwind, but well below the 44.4% peak margin of 2012. While at scale, heatsticks look likely to be higher margin than combustible cigarettes under current favourable tax structures, we believe that in the long run, there will be equitable tax treatment of all tobacco products, which will limit the manufacturers’ margins. The customer acquisition cost is likely to be higher in the emerging categories than in cigarettes, and we assume an incremental 200 basis points of spending on research and development and advertising in our base case, versus the traditional cigarette algorithm. In the long term, further margin degradation is likely to occur from the steady decline of cigarette volumes. However, with 44 manufacturing facilities in operation, PMI has plenty of scope to cut fixed costs, which could help support margins for several years.

We assume a midcycle organic growth rate of 2.6%, with strong pricing of 4%-5% mitigated by low-single-digit volume declines. Assuming the iQOS range is marketed to existing adult smokers, it seems unlikely that volume trends would shift materially as smokers migrate to heated tobacco, so our volume decline assumption of negative 2% is similar to recent trends in the combustible business. Pricing power, however, is likely to be as strong as the combustible business, and we think 4% price/mix is appropriate, as this is consistent with the cigarette business and is stronger than most categories in consumer staples.

Risk and Uncertainty | by Philip Gorham Updated Mar 12, 2019

Our uncertainty rating for Philip Morris International is low. Evidence from the recent economic volatility suggests that industry fundamentals–and, therefore, manufacturers’ cash flows–remain stable. With pricing power intact, the greatest operational risks, in our view, are the risk of more widespread plain packaging measures in large markets and foreign exchange risk.

Any investor owning tobacco stocks should have the stomach for fat-tail risk such as the recent CAD 13 billion judgment against the industry in Quebec, Canada. Litigation risk is substantially lower for the European players, as most countries do not have a class-action legal process. Nevertheless, we regard government and legal risks as low-probability events with high potential impacts that investors should be aware of.

In general, we believe government regulation does little to affect the economic moats or the cash flows of tobacco manufacturers, and in some cases, regulation actually limits competition, lowers cost, and strengthens pricing power. Plain packaging is different, however: We believe that it could facilitate trading down, which would erode pricing power and be detrimental to moats in the industry. Australia introduced plain packs in 2012, and the U.K., Ireland, and France followed suit in 2017. If plain packages are introduced in any other major EU market, this could be materially detrimental to the firm, given its positioning in premium categories.

Philip Morris’ functional currency is the euro, but it reports in U.S. dollars. It also has exposure to currencies too small to hedge in large amounts on the open market. Although it has something of a natural hedge, with about 26% of its costs in euros almost offsetting the 32% of its revenue that is denominated in euros, strength in the U.S. dollar can have a significant and detrimental impact on Philip Morris’ earnings, and this risk has been evident in recent years.

Stewardship | by Philip Gorham Updated Mar 12, 2019

Our stewardship rating for Philip Morris International is Exemplary. We think that the capital allocation of the business has been commendable and that the business is being run for the long-term benefit of shareholders.

PMI’s recent shareholder return performance has been outstanding, with at least 9% annualized returns each year over the past three years. Although the five-year return looks less appealing, returns were weighed down by the removal of the share-repurchase program and currency weighing on operating performance. Management is sometimes criticized for the aggressive nature with which it repurchased shares following the split from Altria in 2008, but given the trajectory of the market capitalization in recent years, it is clear that the buybacks created value for long-term shareholders. We understand that management is prioritizing the maintenance of its investment-grade credit ratings, but we think the recent weakness in the market value of the company presents an opportunity to create further value share repurchases.

Since the rotation of some senior executives, most notably Louis Camilleri stepping aside as CEO in May 2013 and being replaced by former COO Andre Calantzopoulos, we think capital allocation has continued to be sound. Share repurchases have been suspended, a decision that we think was prudent given the strength of the currency headwind. We prefer that free cash flow be allocated to increasing the dividend, a policy management has pursued despite the temporary inflation in the payout ratio, albeit at a slower pace than we think the company can achieve in the medium term. Share repurchases are likely to return when currency headwinds abate and the payout ratio returns to a normalized level in the mid-80s.

The advent of e-cigarettes is presenting the tobacco industry with its greatest upheaval in a generation, and amid this challenge, we believe Philip Morris has allocated internal capital in an effective manner. Management has made a big bet on heated tobacco, having built a $2 billion plant in Bologna, Italy, and taking an industry-leading role in taking the category to market. The heated tobacco category better matches smokers’ preferences than other e-cigarette categories, in our opinion, and we think this will lead to greater consumer adoption. Philip Morris’ investment in iQOS, therefore, gives it early leadership of the category and sets the firm up well for long-term growth.