A mi me parece muy bueno el tipo y soy un accionista bien feliz con lo que hacen desde mediados de este año, dio una muy buena oportunidad en los 48-60 dólares y estuve cargando. No es mi inversión típica, veo que tiene más riesgo pero me gusta lo que hacen. He escuchado bastantes de sus últimas calls desde 2020 y el tipo lo tiene bien claro. No me gusta tanto la sobreexposición que tienen pero entiendo que al no poder atraer institucionales, tienes que intentar atraer el capital del minorista. Bueno, es un precio a pagar. Mi mayor miedo aquí es la gran dependencia de Langan, no se hasta que punto si algo le pasa a el, esa estructura va a seguir funcionando bien. Parece que tienen buenos operadores en los clubes, pero el es la cabeza de todo el tinglado y ahí tienes una gran dependencia de una persona.

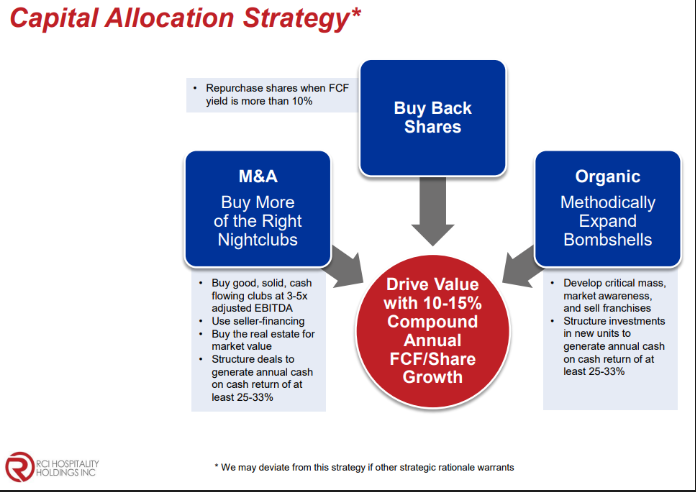

Para empezar, buybacks si, pero cuando estemos cotizando a un FCF yield de más del 10%.

Y si cotizamos más caro, entonces necesitamos adquisiciones y podemos emitir acciones para adquirir eso que queremos, que además nos sirve casi como un crédito que luego podemos ir devolviendo recomprando acciones cuando estén más baratas.

Aunque la joya que tienen es el negocio de los clubes. Tienes algo que parece que los private equity no quieren y puede ir comprando más barato que la emisión de tus acciones:

Why sell at 3x-5x EBITDA?:

Why do guys sell for three to five times EBITDA? Because private equity and banks do not lend money for the acquisition of adult related businesses, are very few in the United States. Other operators do not have access to capital and the capital structure that RCI has. Because of our large real estate holdings, we’re able to borrow money from banks against our real estate, pull out equity, use that equity to buy and pay cash down in large sums, anywhere from $10 million in this last transaction, we paid out, $5 million a transaction up to 30 some million in the Lowrie transaction. And we’re able to use $30 million equity in that transaction as well.

¿Qué nos suben los costes de la construcción de Bombshells y tenemos opciones de adquirir clubes (que es el mejor negocio con diferencia)? Pues hay que hacerlo:

Slowing down Bombshells, transition to Nightclubs:

you’re obviously slowing down Bombshells growth because the ROIs are not there. I don’t like that. I love that. I mean, it’s so perfect, right? It shows the flexibility of mind, that the reality is materials costs are up. Inflation is up, labor is up like, why not be a buyer of these clubs at lower multiples. You own the real estate. In fact, these are the best inflation adjusted assets and you’re the only owners of them. I mean, I would be – I think it’s amazing that you’ve transitioned to focusing on clubs again, it shows a flexible mind. And that our focus is about 95% on clubs and about 5% on Bombshells right now. Because I do think in the next three months that there’s going to be some great opportunities for us on the club side, based on some of my conversations with guys right now, with our hire. We paid three times forever, or less for a long time, many years. We’re starting to pay four to five times right now for the big guys, for the limited clubs, for the right licenses, in the right markets and buying that market share up. And it has got a lot of guys talking to us right now. And I think we’ll bring some of those guys onto our side of the equation soon, rolling up additional thought amounts of EBITDA.

Aquí ya veía oportunidades que iban a llegar en clubes, pues no quemó toda la leña en buybacks, voy comprando y me reservo mis 30-40 kilos para cuando lleguen las oportunidades de adquisiciones.

Y cuando allá por 2013 no podía comprar clubes, pues entonces se inventó el concepto de Bombshells, que no es que sea nada novedoso pero te sirve para invertir el FCF que te vaya generando el negocio de los clubes.

Aunque lo que más me asombra es como sobreviven al COVID, con lo que ello conlleva para el negocio, y cuando sacan la cabeza se marcan la adquisición más grande de la historia de la empresa.

En fin, que estamos infravalorados toca quemar en buybacks. Que estamos más sobrevalorados, toca emitir acciones y comprar cositas. No se, mas allá de todo esto, es tener un capital allocation marcado que tenga sentido y ejecutarlo, y no andar cambiando cada 2 años de plan estratégico: