Venderéis una parte para invertir en otras o dejáis correr las ganancias?

Con que criterio quitaréis una empresa de la cartera?

Venderéis una parte para invertir en otras o dejáis correr las ganancias?

Con que criterio quitaréis una empresa de la cartera?

Vender un bagger?? Eso es un pecado mortal, a no ser que uno sea funcionario de Hacienda…

En todo caso, se venderían los malos negocios, para reforzar los buenos, cuando estén de rebajas.

Una empresa se debe quitar de la cartera, cuando el negocio deja de ser excelente, o peligra gravemente no por un tema coyuntural, sino estructural. Si la selección previa es buena, esto es raro que ocurra.

Después otra duda, empecé una cartera dividida por capitalización. Con lo q ahora tengo compañías con 4% y 6% en lugar de 2%, venderíais el excedente o lo dejariais hasta que aumente el tamaño de la cartera?

PD: Si es offtopic, movedlo.

En la cartera particular, yo solo vendo por temas fiscales para compensar ganancias con alguna en pérdidas. Si una empresa excelente es el 6% no hay problema. Si el 6% es Purford o similar, yo me preocuparía…

Si la que ocupa un 2% es excelente, hay que tratar de incrementarla.

Las Valoraciones, cuando acabe el curso, a 31 de diciembre. No conviene malgastar saliva y neuronas…

La virtud de no hacer nada.

Compra empresas de calidad y éstas (a largo plazo) harán su trabajo.

El índice +D51 sigue al tran tran, sin rotación alguna desde sus inicios, y sin necesidad de cambiar de índice con quien compararse para disimular o parecer mejor que nadie.

A pocas semanas de cerrar el año, un 30,57% contando dividendos (a estas alturas ya están casi todos pagados), o si lo prefieren 28,63% sin dividendos.

Top 10:

| Valor | Ticker |

|---|---|

| Mastercard | MA |

| Microsoft | MSFT |

| Apple | AAPL |

| Blackstone | BX |

| Visa | V |

| Danaher | DHR |

| Airbus | EPA:AIR |

| LVMH | EPA:MC |

| Amazon | AMZN |

| Dassault Systemes | EPA:DSY |

y para que vean que no todo son historias de éxito, el Bottom 10:

| Valor | Ticker |

|---|---|

| Anheuser Busch | BUD |

| Viscofan | BME:VIS |

| Henkel | ETR:HEN |

| Altria | MO |

| Daimler | ETR:DAI |

| Burelle | EPA:BUR |

| British American Tobacco | BATS |

| Gilead | GILD |

| Plastic Omnium | EPA:POM |

| Pandora | CPH:PNDORA |

Señores, nada más que decir.

Buenas noches.

Increíble el rendimiento de la cartera.

Por cierto, con quién debería hablar para conseguir esa plantila?

Gracias

Pues en el bottom 10 hay alguna interesante… BATS, Gilead, Altria…

¿Algún valiente se atreve a realizar una tesis de inversión en Gilead? Lleva unos años duros, siempre parece barata pero…

A favor de Gilead, @Helm y un servidor. En contra @Fernando .

Al final ganará Fernandito, pero Helm y yo le daremos batalla

Y si no recuerdo mal, a favor de Gilead también están los algoritmos de Adarve Altea…

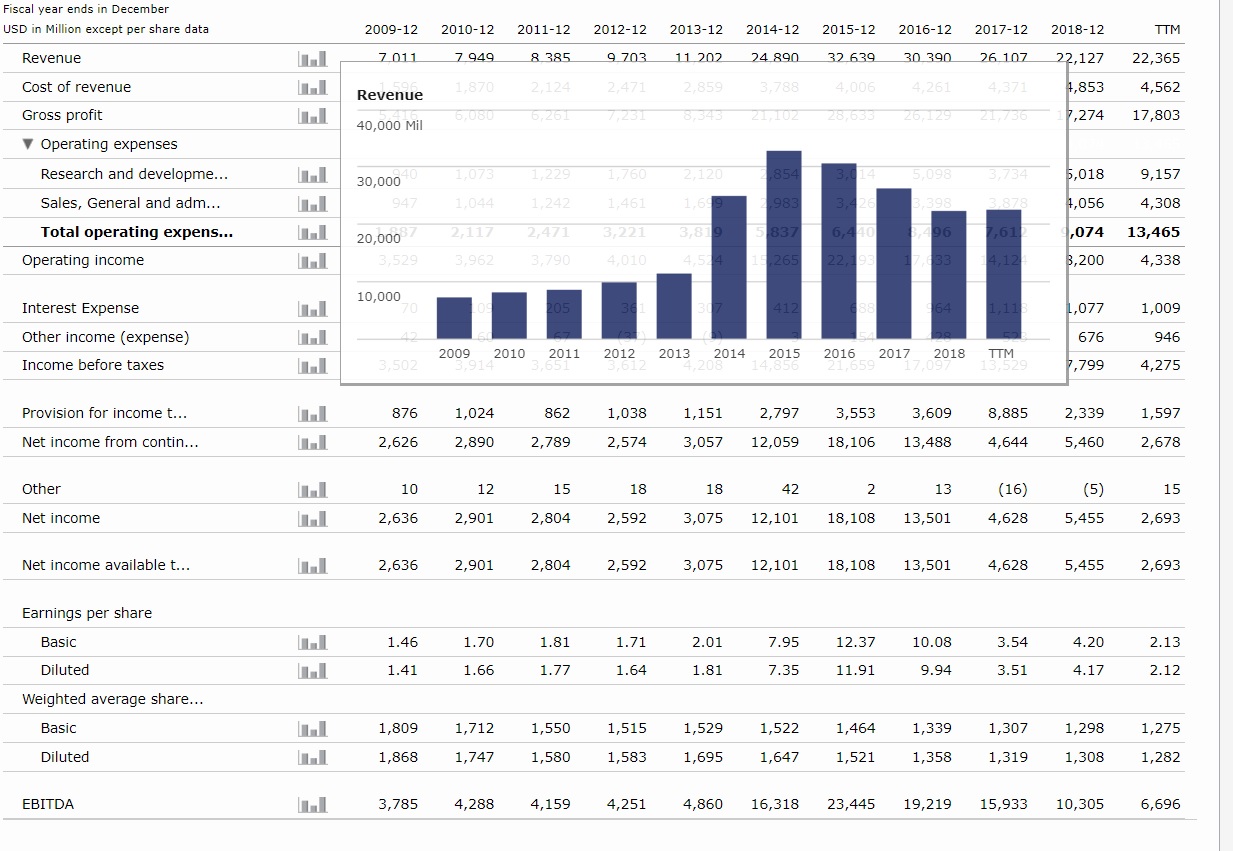

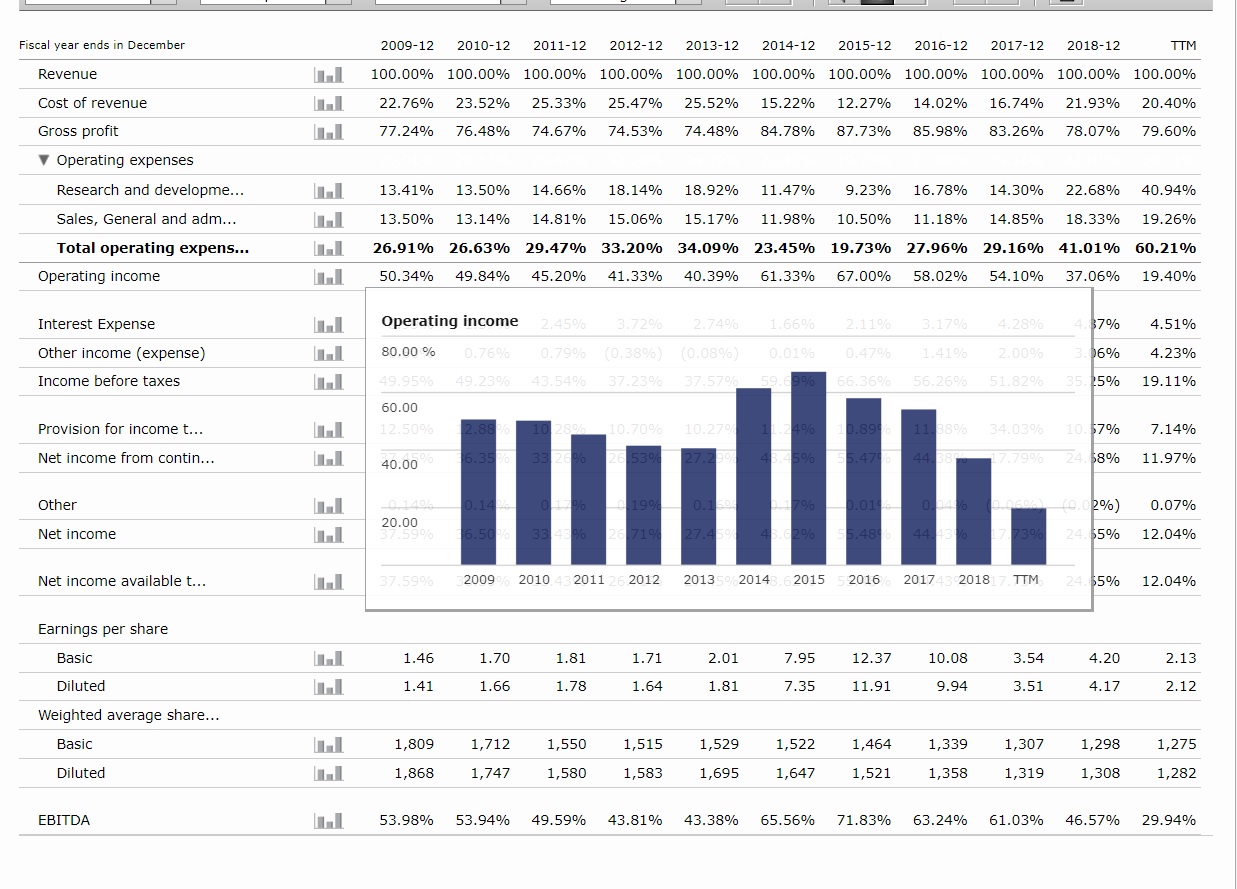

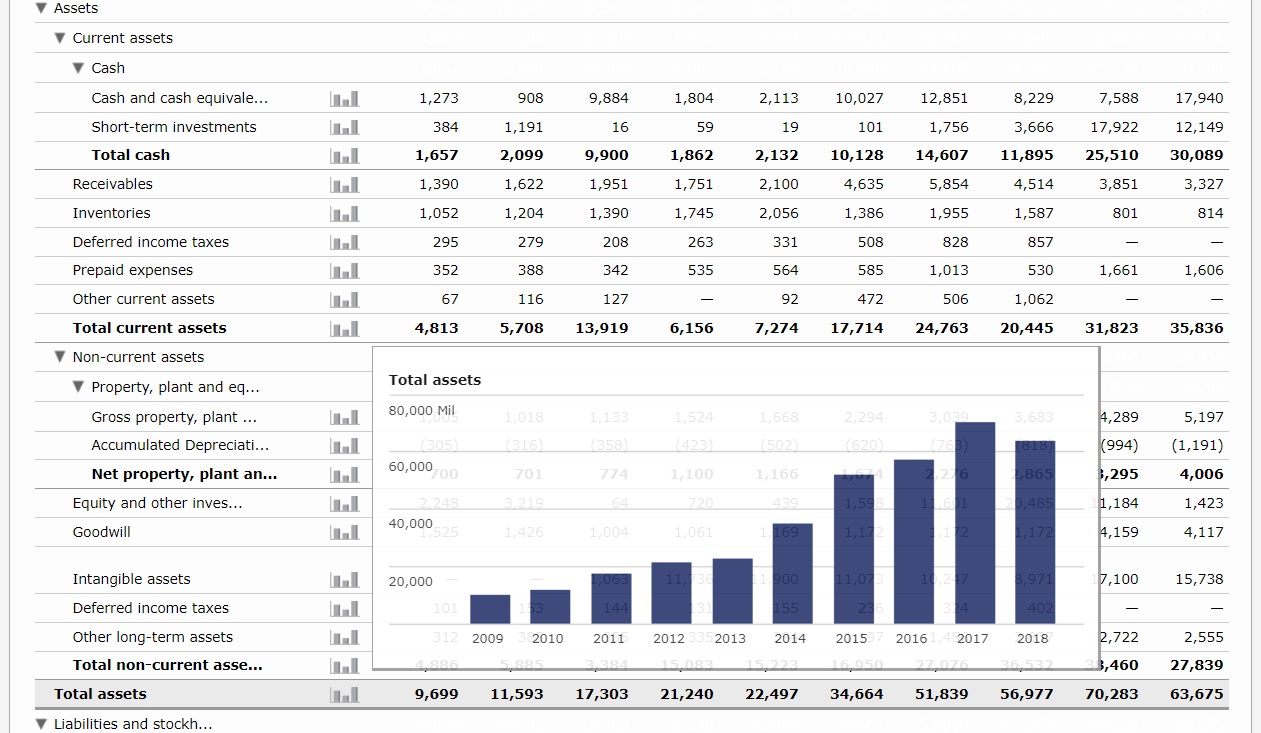

GILD

Ventas:

Márgenes:

Activos:

Para un earnings yield del 11%.

De nuestros amigos de M*, espero que no les importe:

Gilead Reports Q3 With Few Surprises; Descovy PrEP and Filgotinib Launches Are Key Catalysts

Analyst Note | by Karen Andersen Updated Oct 25, 2019

We’re maintaining our $84 per share fair value estimate for Gilead following an in line third quarter, and we remain bullish on uptake of Descovy in HIV prophylaxis as well as long-term potential for immunology drug filgotinib in rheumatoid arthritis (2020 launch) and other indications (2020 ulcerative colitis data). The strength of Gilead’s HIV portfolio led to 13% HIV sales growth, and the launches of TAF-based HIV treatments and prophylaxis regimens should continue to support share gains from competitors like Glaxo. Filgotinib has been filed with regulators in Europe and Japan, and with a U.S. filing coming later this year, we think the drug is on track for a late 2020 launch with a differentiated safety and efficacy profile (although a class-related black box warning related to thrombosis is likely). Shares remain undervalued, and we expect these two products are key to improving investor sentiment. Gilead’s wide moat, which has roots in a strong virology franchise, is also supported by pipeline progress in immunology and oncology.

That said, we expect continuing underperformance in cell therapy and hepatitis C, and NASH remains a wild card where we have conservative expectations following selonsertib’s phase 3 failure. Flat quarter-over-quarter sales of cell therapy Yescarta are consistent with our long-term conservative expectations for Gilead’s CAR-T franchise, due to competition from other CAR-T therapies in clinical trials as well as Roche’s newly-approved therapy Polivy. In addition, the 25% decline in hepatitis C franchise sales matched our estimates, although we expect pricing pressure and share losses to lessen beyond 2020. Gilead expects phase 2b data for a two-drug NASH combination by the end of the year, and although we don’t model sales in NASH for Gilead until 2023, we think potential efficacy could also come from the in-progress combination with Novo Nordisk’s diabetes therapy semaglutide (data expected in the second half of 2020).

Business Strategy and Outlook | by Karen Andersen Updated Jul 31, 2019

Gilead generates stellar profit margins with its HIV and HCV portfolio, which requires only a small salesforce and inexpensive manufacturing. We think the firm’s portfolio and pipeline support a wide moat, but Gilead needs HCV market stabilization, strong continued innovation in HIV, solid pipeline data, and smart future acquisitions to return to growth.

Gilead’s tenofovir (TDF) molecule–in Viread, Truvada, and older single-tablet regimens–historically formed the heart of the firm’s $15 billion HIV franchise. Combo pills offer convenience and affordability, as patients are less likely to miss doses and develop drug resistance, and they only need to make one copayment. The newest combo pills–replacing TDF with TAF–reduce bone and kidney safety issues and are seeing rapid uptake. Gilead’s biggest competitive threat in HIV is Glaxo; Triumeq saw rapid growth in 2015, and Glaxo is launching two-drug regimens based on its integrase inhibitor Tivicay (Juluca in 2017 and Dovato in 2019) that also bypass Gilead’s drugs. However, Gilead’s Genvoya (2015), Odefsey (2016), Descovy (2016), and Biktarvy (2018) launches push patent protection into the late 2020s and are boosting Gilead’s market share.

The $11 billion Pharmasset deal brought key HCV drug Sovaldi. Sovaldi and Harvoni (a combination of Sovaldi and ledipasvir) peaked at more than $19 billion in sales in 2015. However, demand has been shrinking as patients are cured, and competition from AbbVie and Merck has led to several rounds of significant price-discounting. We expect Gilead and AbbVie to share a $5 billion-plus market in the long term.

Gilead is building a pipeline outside of HIV and HCV but will need more acquisitions like Kite (with CAR-T therapy Yescarta) to see strong growth. Gilead’s first cancer drug, Zydelig, launched in 2014, is limited by safety concerns, but we’re more optimistic about the firm’s immunology portfolio, including JAK1-inhibitor filgotinib from the Galapagos collaboration. Lead NASH program selonsertib recently failed in a phase 3 trial, but Gilead has an ongoing midstage trial exploring combination therapy with other mechanisms in NASH.

Economic Moat | by Karen Andersen Updated Jul 31, 2019

We assign Gilead a wide economic moat rating. We think patent protection on newer HIV regimens and Gilead’s continued dominance in the hepatitis C market will be enough to ensure strong returns for the next couple of decades. Gilead’s expertise in infectious diseases and single-pill formulations is a part of its research and development strategy, which we see as one of the strongest intangible assets supporting the firm’s wide moat.

Gilead’s moat was formed by its leadership position in the treatment of HIV, with patented products that form the backbone of today’s treatment regimens. Despite numerous competitors, the company has established leading market share and spectacular profitability with its convenient, effective, and safe treatments. Gilead serves 80% of treated HIV patients in the United States. Management has done an excellent job of maximizing sales of the TDF molecule, which is present in Viread, Truvada, Atripla, Complera, and Stribild. That said, key patents are beginning to expire in Europe, and next-generation products could struggle to provide sufficient differentiation for reimbursement in all key markets. This puts pressure on the HIV franchise beginning around 2021.

However, we think the firm has shown that it can translate its extensive understanding of the drug discovery and development process in HIV into new therapeutic areas, allowing it to achieve wide-moat status. Despite initial criticism of the high price that Gilead paid for Pharmasset in early 2012, the $11 billion acquisition gave Gilead the most valuable hepatitis C drug in the industry and also demonstrated the firm’s ability to recognize the potentially unique nature of Sovaldi’s safety and efficacy profile compared with other, toxic nucleotide analogs. We think the firm’s experience with another nucleotide analog, tenofovir, a key ingredient in all of Gilead’s HIV combination regimens, probably contributed to its recognition of Sovaldi’s value at an early stage in its development.

The molecule in Sovaldi and Harvoni has redefined Gilead as a powerhouse in the broader infectious disease market. Gilead is leading the way for all-oral treatments in the hepatitis C market, and it has a multi-billion-dollar product. We think the low resistance potential and pan-genotypic efficacy of Gilead’s regimens will allow the firm to retain close to 40% of the global HCV market in the long run, despite competition from AbbVie and Merck.

Fair Value and Profit Drivers | by Karen Andersen Updated Jul 31, 2019

We’ve raised our fair value estimate to $84 per share from $78 as we’ve increased our Biktarvy sales assumptions following its rapid launch (partly countered by lower sales of older regimens like Genvoya and Atripla) and also increased forecast for filgotinib, with a higher 80% probability of approval in rheumatoid arthritis.

We still assume Gilead’s HCV business will fall below $3 billion in 2019, with annual declines stabilizing around 10% beyond 2019.

We think Gilead’s HIV/HBV franchise will peak at $19 billion in 2021, with U.S. generic competition leading to a high-single-digit annual headwind beginning in 2022. We now assume that all TAF-based combination regimens (Biktarvy, Genvoya, Descovy, and Odefsey) will help offset declines, but that Gilead could see mid-single-digit patient losses in the U.S. annually beginning in 2022. We still view Stribild and Complera generics as strong long-term competition for TAF-based regimens, particularly outside the U.S.

Overall, we forecast 1% sales growth and 4% non-GAAP earnings growth through 2023. Sovaldi and Harvoni’s high gross margins, strong operating leverage, and lower tax rate led to a 68% operating margin in 2015, and with shrinking revenue, we think these margins will stay in the 40s going forward. We assume that cost-cutting will help offset margin pressure.

We include $1.3 billion in sales from Yescarta by 2023, with annual sales stabilizing around this level as usage expands to second-line DLBCL therapy and other forms of blood cancer, but the competitive landscape gets tougher.

We assume a 6.8% cost of capital for Gilead. We rate the systematic risk surrounding Gilead shares as below average and assume a cost of equity of 7.5% to align our capital cost assumptions with the returns equity investors are likely to demand over the long run. We also assume a 5.5% pretax cost of debt to reflect a more normalized long-term rate environment.

Risk and Uncertainty | by Karen Andersen Updated Jul 31, 2019

Increasing competition and pricing pressures in the HIV and hepatitis C markets are risks for Gilead. Global pricing pressure and consolidation of pharmacy benefit managers could reduce Gilead’s ability to charge price premiums for new drugs or extend patent protection. If Gilead’s newest HIV products aren’t perceived as offering significantly improved safety or efficacy versus its older HIV products, a large portion of its sales foundation could be at risk. Key patents on Gilead’s top marketed HIV products will expire by 2021, and the firm will need to see significant switching to newer products like Biktarvy to counter the negative impact from generic competitors. We estimate that more than 60% of Gilead’s U.S.-based HIV sales volume represents government purchases, and higher rebates on some of these sales were implemented in 2010. Escalating overall healthcare costs and tight budgets could lead to continued, elevated pricing pressure in both the U.S. and Europe. Gilead also paid a significant premium to acquire Myogen, and the failure of darusentan put pressure on Letairis to make the deal accretive. The $11 billion Pharmasset acquisition, the foundation for Gilead’s HCV franchise, allowed Gilead to generate more than $19 billion in HCV revenue in 2015 alone, but Gilead’s HCV business has declined steeply since 2016, as competition allowed pharmacy benefit managers like Express Scripts to aggressively negotiate pricing. Gilead and AbbVie continue to compete on price. In HIV, Express Scripts could exclude newer HIV products from its formularies once safe and effective competition–like Gilead’s own Atripla and Complera–lose patent protection. Glaxo’s two-drug regimen could also put pressure on pricing, and payers could get more creative, offering financial incentives for patients to take new combinations as patents expire.

Stewardship | by Karen Andersen Updated Mar 27, 2019

Our stewardship rating for Gilead is Standard as the firm undergoes a management transition and as we await details on any changes to strategy or performance. Previously, we have applauded Gilead’s moat-building investment strategies, good allocation of capital, and superior board independence and qualifications.

Gilead’s 2018 was a year of massive management turnover, and while we think the hiring of Roche’s Daniel O’Day as the new chairman and CEO (effective March 1, 2019) adds stability, we’re concerned that the firm might still lack the scientific expertise needed to guide accretive mergers or acquisitions, given O’Day’s marketing background. Significant turnover gives the firm the opportunity for a fresh management team to enter at a time when massive revenue headwinds from the HCV franchise are abating, but we think it is too early to assume it can live up to the prior Martin/Milligan team’s record. We see blood cancer and immunology as key areas of future growth for Gilead, which both fit well with O’Day’s prior experience at Roche. However, Gilead’s current reliance on its core HIV portfolio for growth puts pressure on both pipeline advancement and the ability to make strategically sound details to support this strategy. While O’Day was at Roche for 31 years and had been CEO of Roche’s pharmaceutical division since the departure of Pascal Soriot in 2012, our window into his ability to make accretive deals is limited (including the $8 billion acquisition of Intermune and the mildly disappointing oral IPF drug Esbriet).

Gilead CEO John Milligan stepped down at the end of 2018, along with board chairman (and former CEO) John Martin. Milligan has spent 28 years at Gilead but had only been in the CEO role since March 2016. This followed chief scientific officer Norbert Bischofberger’s departure at the end of April 2018 and chief medical officer Andrew Cheng’s departure in September 2018. Milligan and Martin were the only insiders on Gilead’s 10-member board, which has an independent lead director. Experienced board members offer a diverse skill set, including expertise in public policy, infectious disease, and global health initiatives. We like that management is rewarded for R&D progress rather than earnings per share. Gilead’s heavy $26 billion in share repurchases during 2014-16 were made at valuations above recent share prices and our current fair value estimate, and the program has shrunk significantly since then, presumably as Gilead saves for potential acquisitions.

Gilead has made several acquisitions and collaborative deals over the years that have supported its infectious disease portfolio. For example, the acquisition of Triangle in 2003 brought Emtriva, a critical component of Truvada and all of the firm’s single-tablet HIV regimens. Outside of Gilead’s therapeutic area focus, the acquisition of CV Therapeutics was also a wise investment, as angina drug Ranexa is growing strongly. In addition, the $11 billion bet on Pharmasset–and hepatitis C drug Sovaldi–was an excellent use of capital. While it is too early to judge the $11.9 billion acquisition of Kite Pharma in 2017, we currently assume the deal is neutral to long-term ROICs; upside is possible if Yescarta uptake is faster than expected or if Kite’s pipeline beyond Yescarta proves lucrative, but downside exists if other CAR-T therapies prove safer or if other treatment modalities (like bispecifics) can offer similar efficacy.

Con esas “peores” ,también se puede vivir . MO,BATS un chorro de dividendos ,cada trimestre.Ahora pagó BATS ,en enero paga MO (y su hermana PM).

No todo van a ser recibos,retenciones a cuenta,etc…lo que entra en la cuenta.

Se que tiene poco valor pero…

Altria Group’s annualized return on invested capital ( ROIC ) for the quarter that ended in Jun. 2019 was 20.65%. As of today (2019-10-31), Altria Group’s WACC % is 3.84%. Altria Group’s return on invested capital is 20.61% (calculated using TTM income statement data).

Si lo que le gana al capital es el 20,7% …y lo que paga por él es el 3.8%, es un negocio que hasta yo lo entiendo.

Con BATS,hay que tener paciencia, y dejar que digiera la Boa esa que compró hace años:Reynolds. Ahora ROIC,el 6%…pero ya volverá al 20% ,en unos años.

Si estas,compraran decentemente y no los truños de JUUL,Reynolds,Kronos…volarían.

Démosle tiempo, que maceren como el buen vino, y veremos si Juul y Kronos son buenos business, o son como Timofónica…

A ver qué día se animan a sacar un fondo , creo que le darían batalla al mismísimo fundsmith.

Enhorabuena por su cartera

Impresionante lo de este portfolio, para mi ha sido muy revelador tanto este tema del foro como el del vague investing. Muchísimas gracias por aportar tantísimo.