Viendo la última que intentaron no estoy yo tan seguro tampoco…

4 Me gusta

Había unos costes de financiación muy bajos en ese momento. Ahora dudo que puedan permitirse pagar un múltiplo tan alto (esperemos).

2 Me gusta

2 Me gusta

2 Me gusta

Pues parece que tenemos nuevo CEO:

4 Me gusta

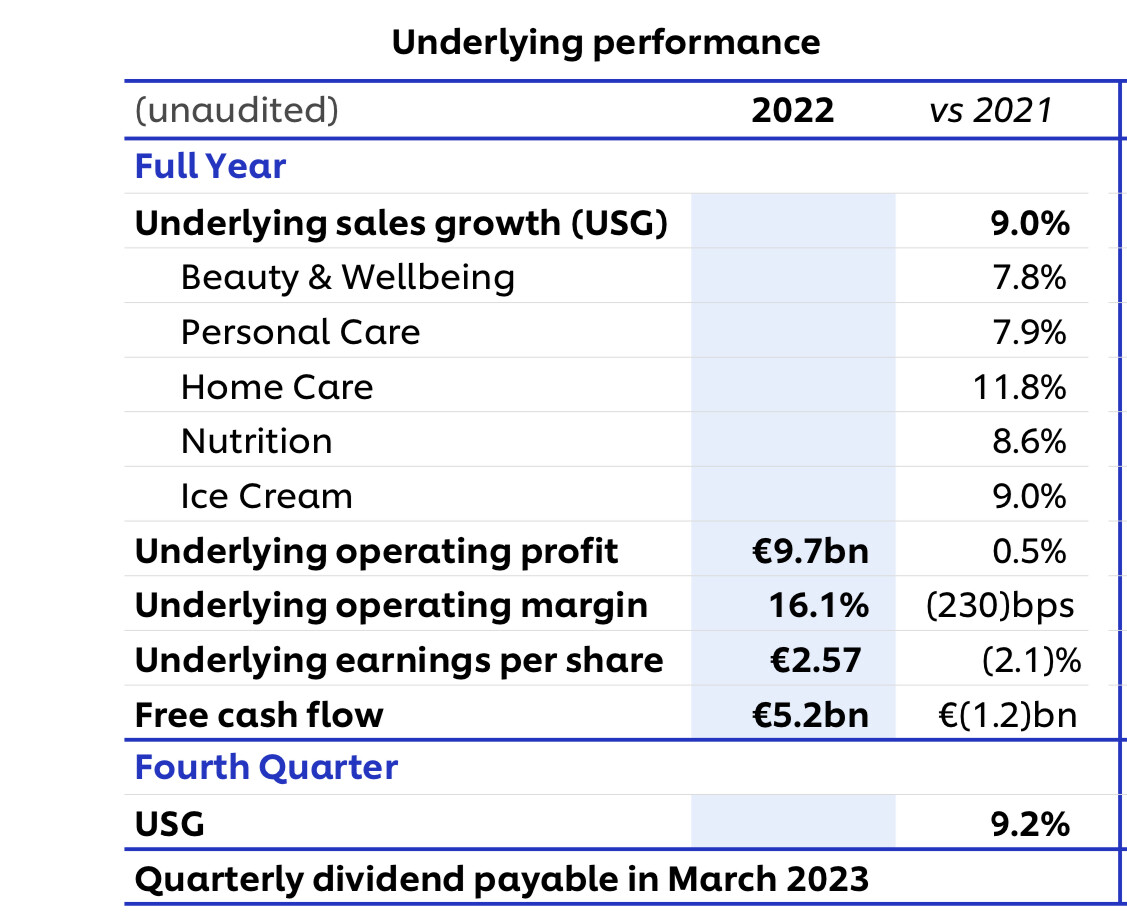

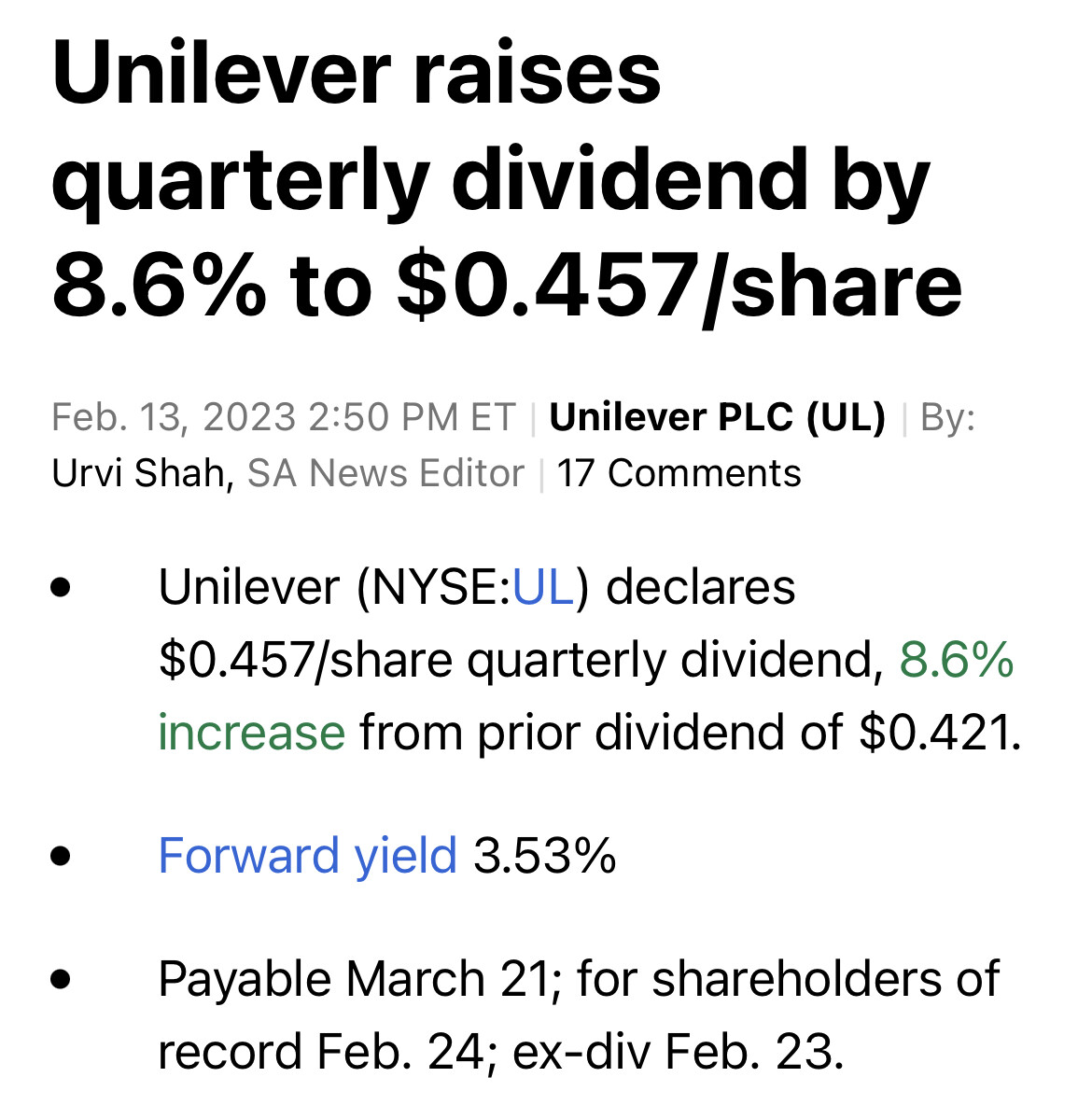

Pues ya tenemos los resultados del año 2022 completos:

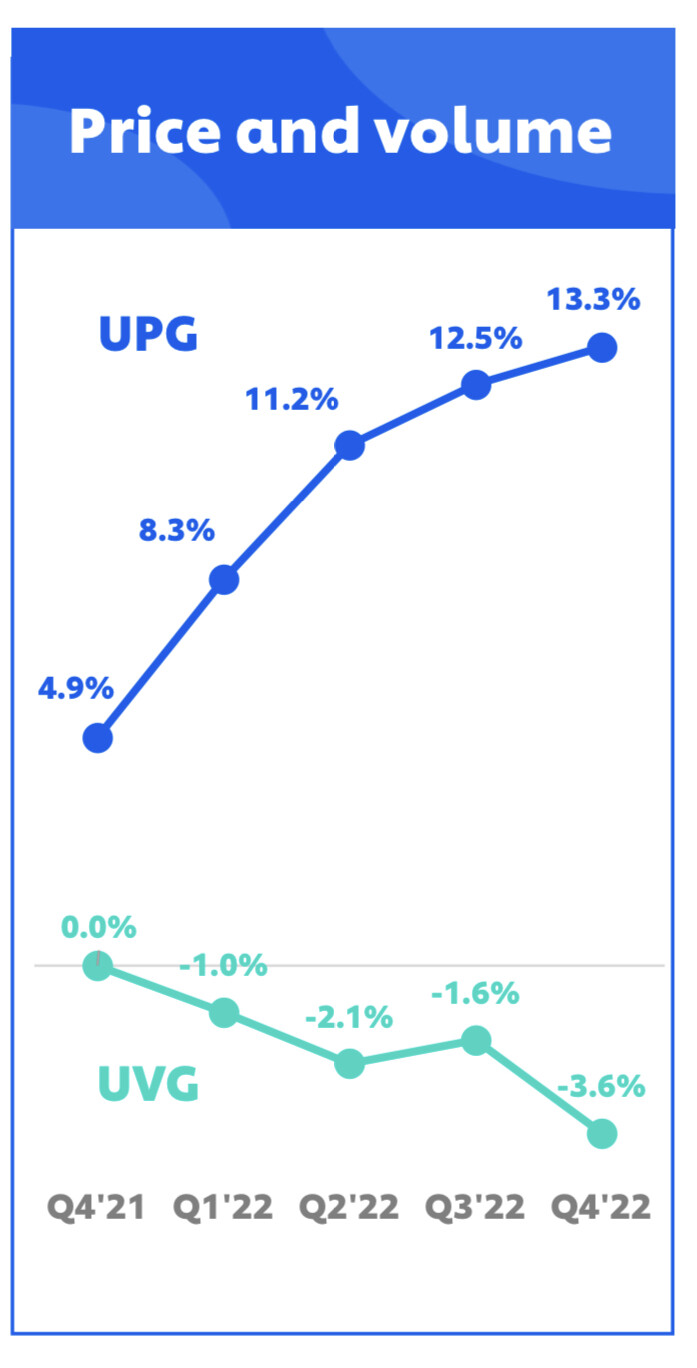

Mantiene beneficios gracias a las subidas de precios. Como consecuencia, caen márgenes.

Entiendo que en parte influirá también por la caída del 2% en volúmenes que ha tenido YoY.

Esto es lo bueno de las defensivas que, cuando vienen tiempos revueltos, defienden ![]()

Asignación de capital:

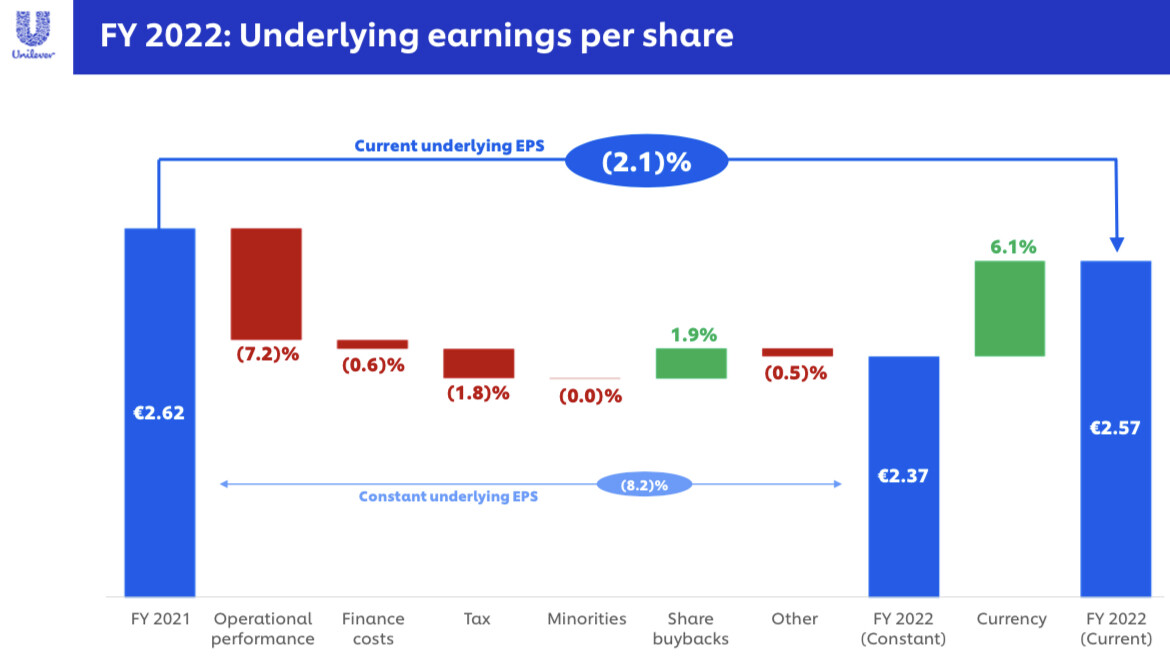

Aquí guidance para 2023 ![]()

In 2022, we carefully balanced price growth, volume and competitiveness to navigate through the high cost inflation environment. We will again deliver strong underlying sales growth in 2023, with improving volume performance and competitiveness as the year progresses. We will continue to price and drive our cost savings programmes, in order to allow us to invest behind our brands and deliver improved margin.

We expect cost inflation to continue in 2023. Our expectation for net material inflation (NMI) in the first half of 2023 is around €1.5 billion. We anticipate significantly lower NMI in the second half, with a wide range of possible outcomes, though we do not expect cost deflation.

In the first half, underlying price growth will remain high, and volume growth will be negative. Volume will improve as price growth softens, but it is too early to say whether volume will turn positive in the second half. We expect 2023 underlying sales growth to be at least in the upper half of our multi-year range of 3 – 5%.

We will deliver only a modest improvement in underlying operating margin in the full year, as we plan for another year of increased investment, and with cost inflation remaining high, underlying operating margin will be around 16% in the first half. In 2022, we carefully balanced price growth, volume and competitiveness to navigate through the high cost inflation environment. We will again deliver strong underlying sales growth in 2023, with improving volume performance and competitiveness as the year progresses. We will continue to price and drive our cost savings programmes, in order to allow us to invest behind our brands and deliver improved margin.

We expect cost inflation to continue in 2023. Our expectation for net material inflation (NMI) in the first half of 2023 is around €1.5 billion. We anticipate significantly lower NMI in the second half, with a wide range of possible outcomes, though we do not expect cost deflation.

In the first half, underlying price growth will remain high, and volume growth will be negative. Volume will improve as price growth softens, but it is too early to say whether volume will turn positive in the second half. We expect 2023 underlying sales growth to be at least in the upper half of our multi-year range of 3 – 5%.

We will deliver only a modest improvement in underlying operating margin in the full year, as we plan for another year of increased investment, and with cost inflation remaining high, underlying operating margin will be around 16% in the first half.

Dicho esto, long Unilever.

Aquí la presentación ![]()

7 Me gusta

A mi me ha parecido significativo esto:

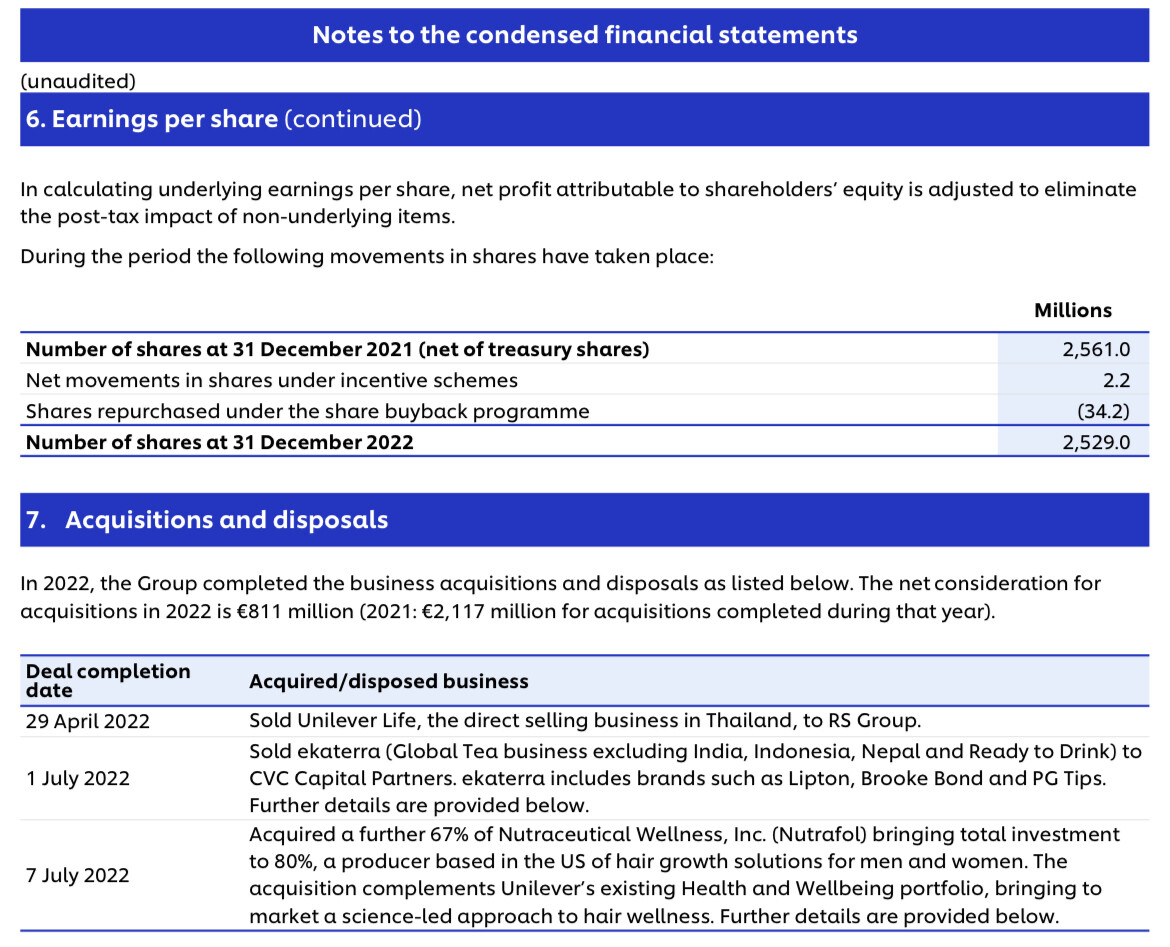

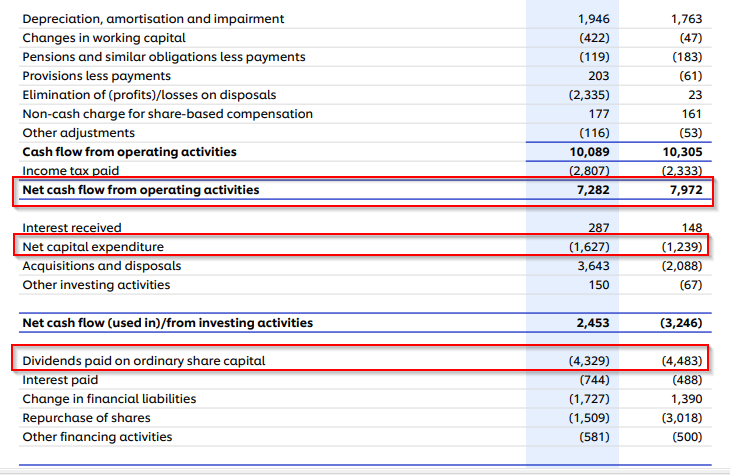

Se han quitado casi un 2% de acciones con el 1.5B€ de recompras que han hecho durante 2022. Y ni aun así han sido capaces de ganar más. Sin las recompras estaríamos hablando de -4% de beneficio. En 2023 imagino que van a hacer otro 1.5B€ que les queda de buybacks y a ver si consiguen ya ganar más. El FCF de 2022 está en 5.6B€. 4.3B€ se te va en dividendos y ya con el 1.5B€ que te queda del programa de recompras ya andas por ahí.

Y aquí vemos el ahorro de 150 millones en pago de dividendos con las recompras y no incremento del mismo:

Esto ahora mismo cotiza como a un 4.5% FCF yield y como a 18x beneficios. Pues bueno, ahí se va. En 40€ como estuvo era otra cosa, a ver si vuelve por ese territorio o son capaces de traducir el crecimiento en ventas al bottom line.

14 Me gusta

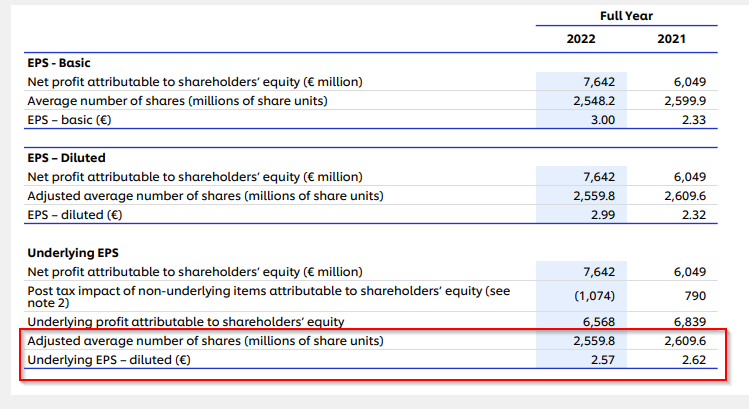

La caída de EPS viene por los márgenes que se han visto impactados por la inflación.

Han pasado de un margen del 18% al 16% y de ahí la caída.

9 Me gusta

La presentación de resultados:

6 Me gusta

¿Unilever no declaraba dividendos en euros?

1 me gusta

Ha visto usted el truco.

Es una “subida” para los inversores en dólares, por la depreciación del dólar ![]() .

.

7 Me gusta

Enlace a KPIs de la compañía interesantes:

2 Me gusta

Qué difícil ha sido para las staples mantener volúmenes. Menuda bestialidad la subida de precios del último trimestre.

2 Me gusta

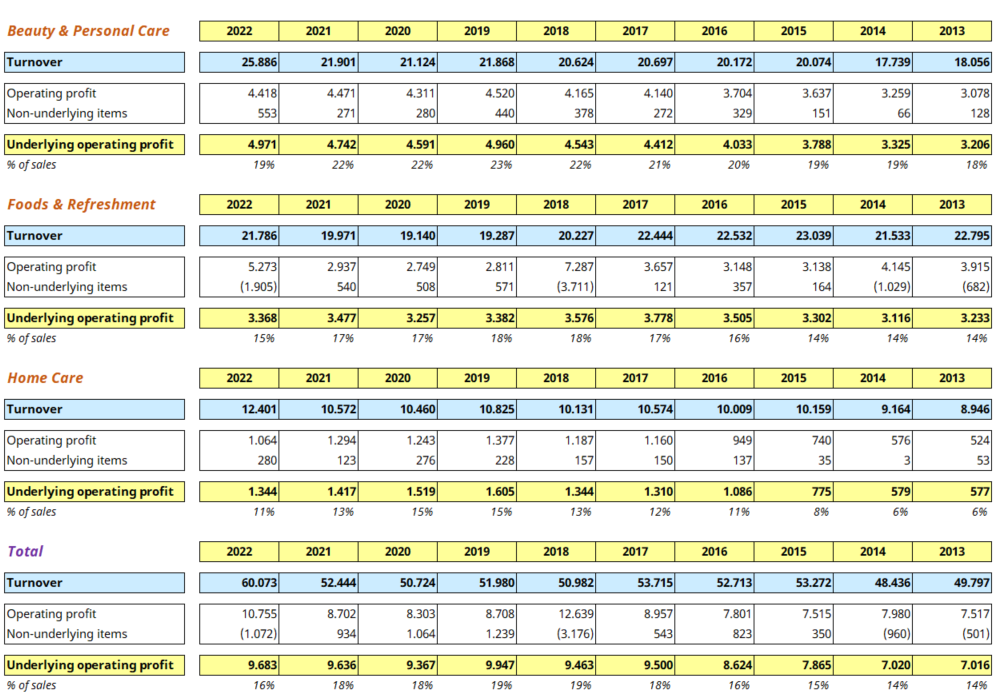

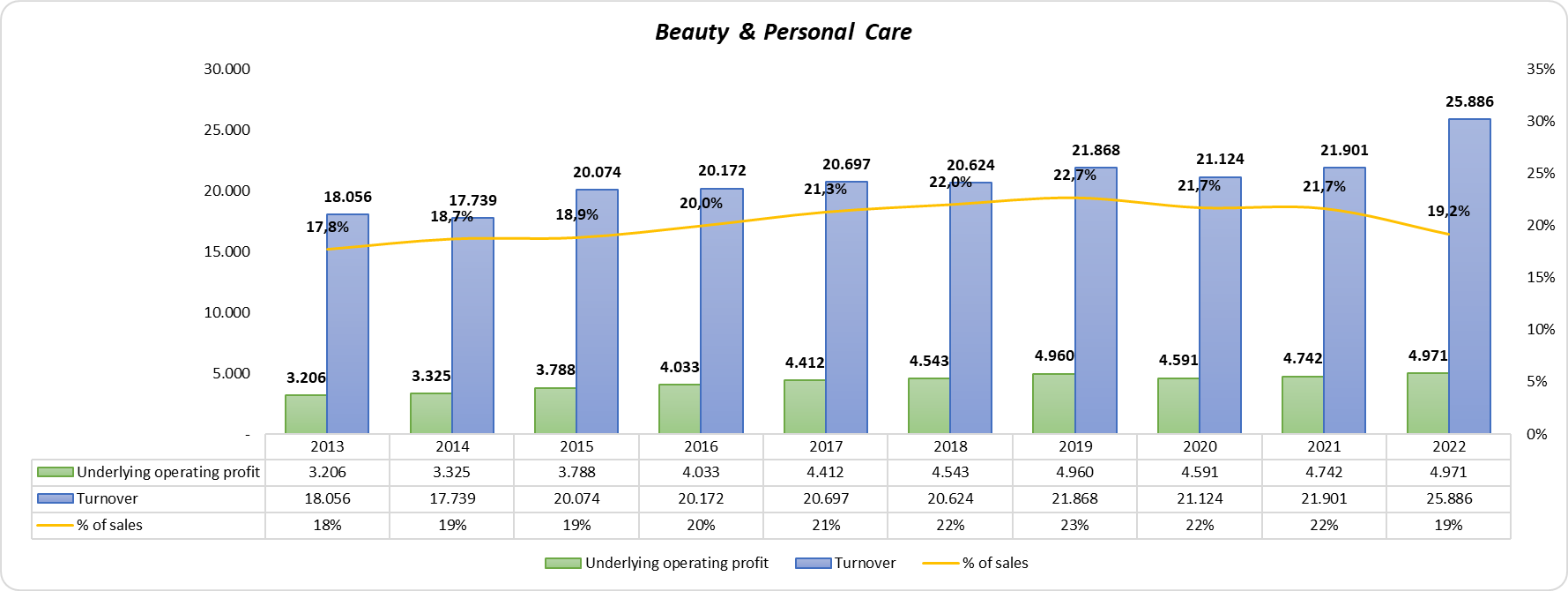

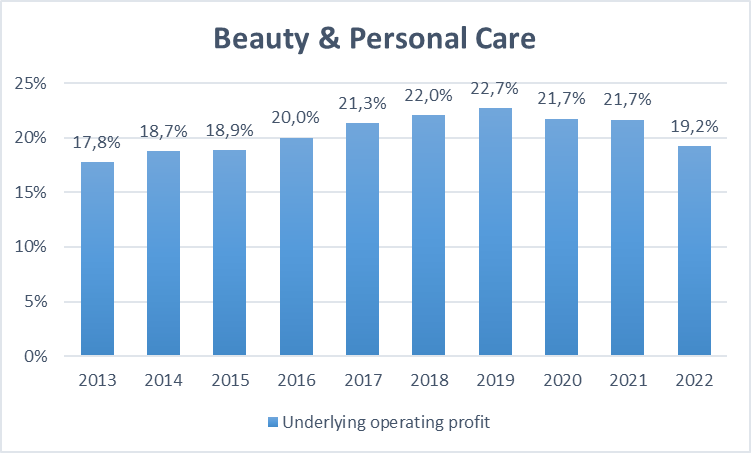

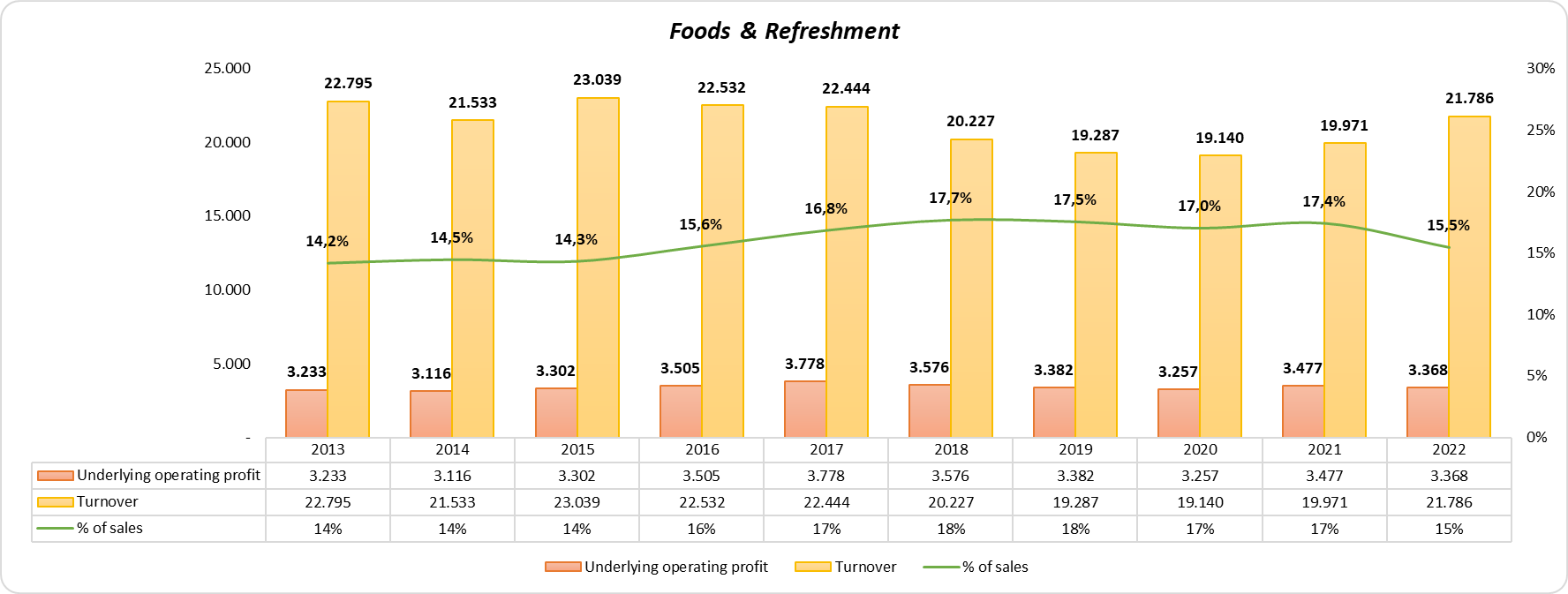

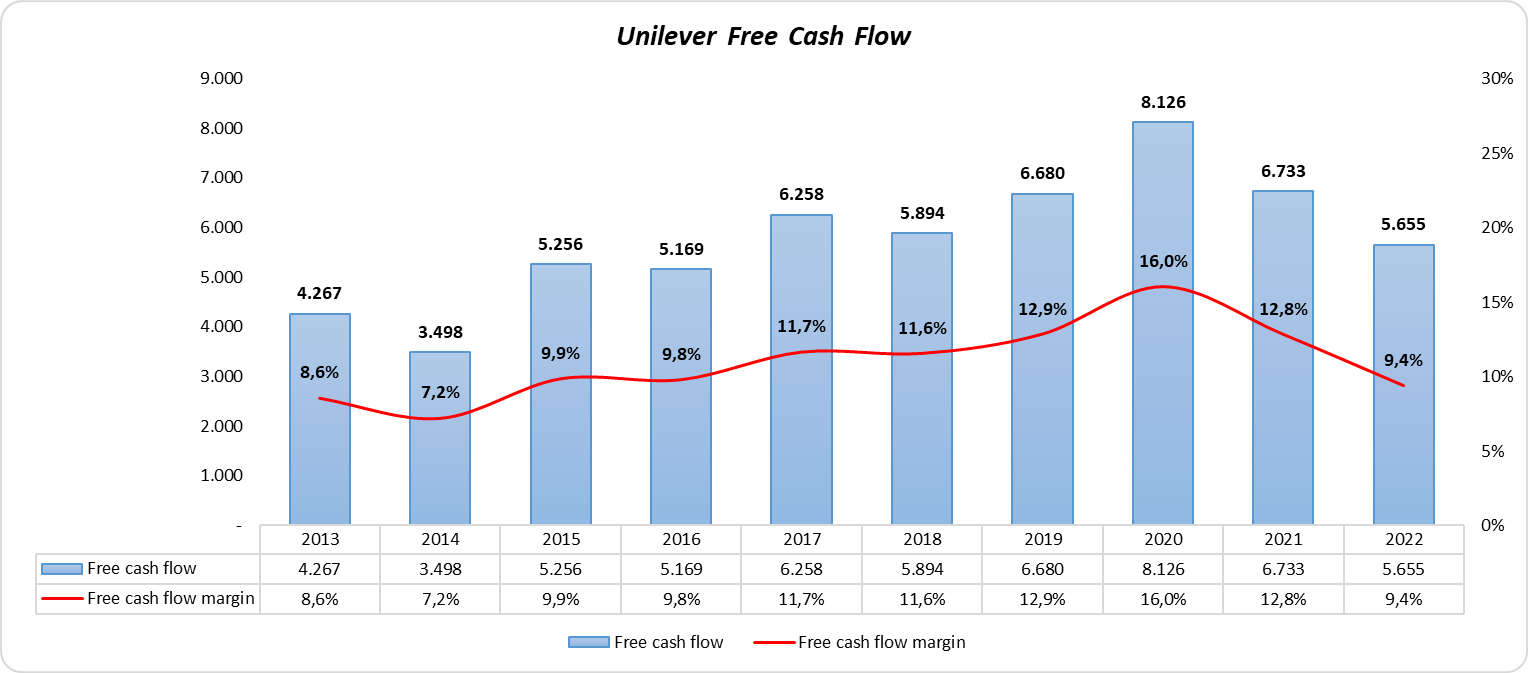

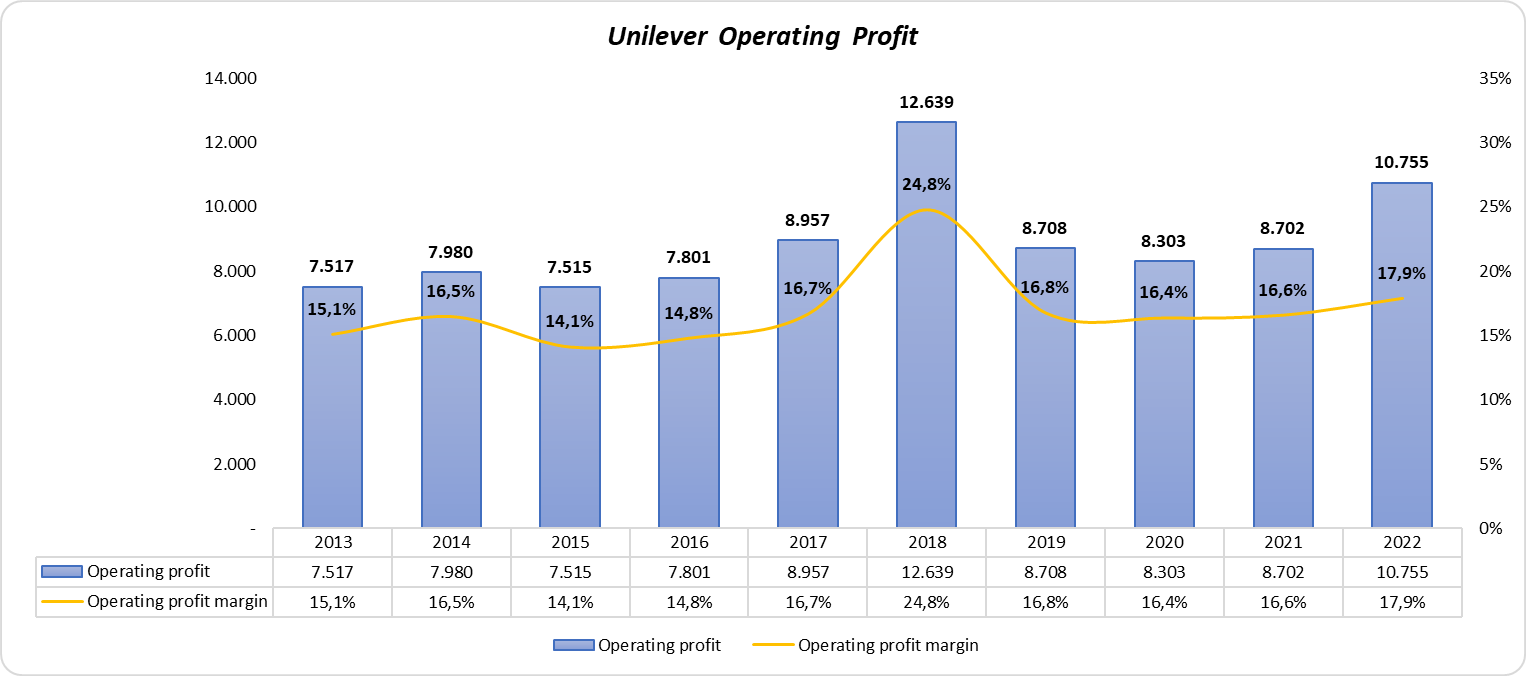

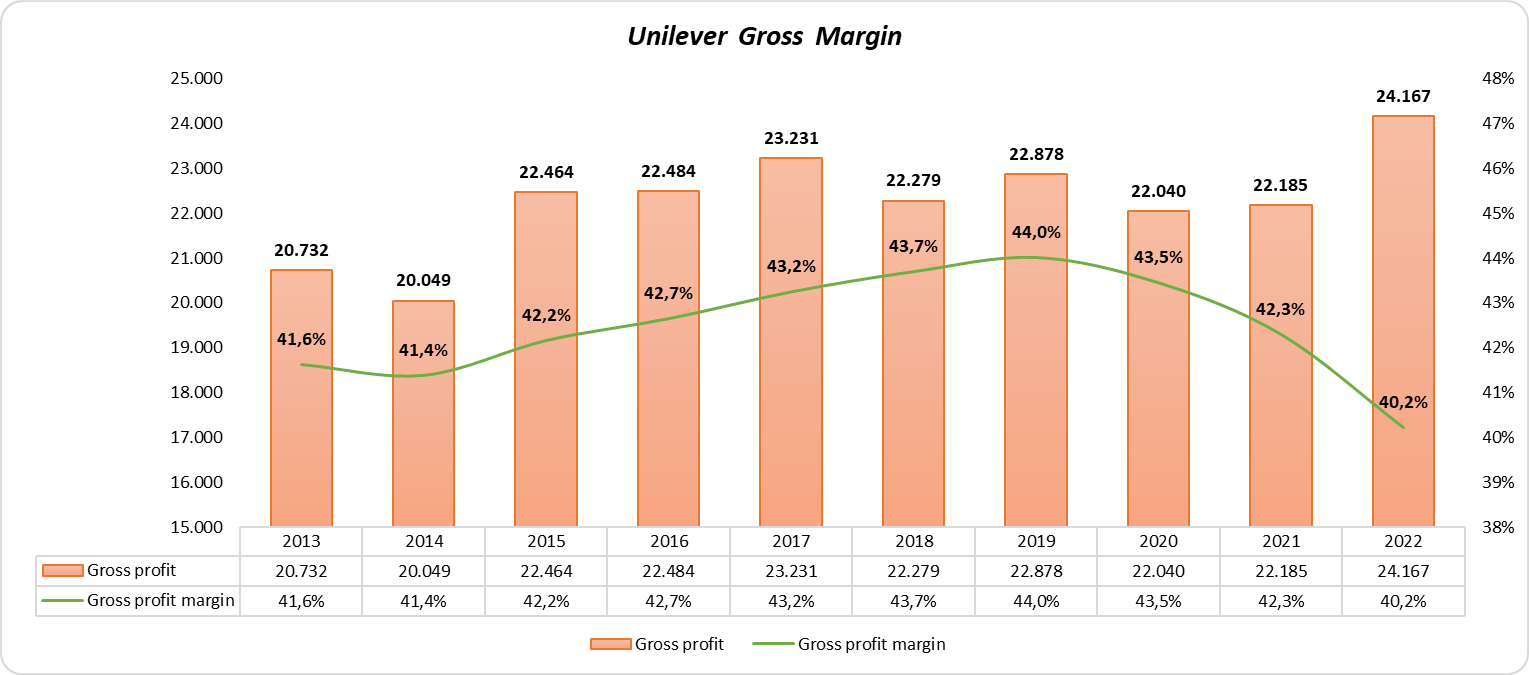

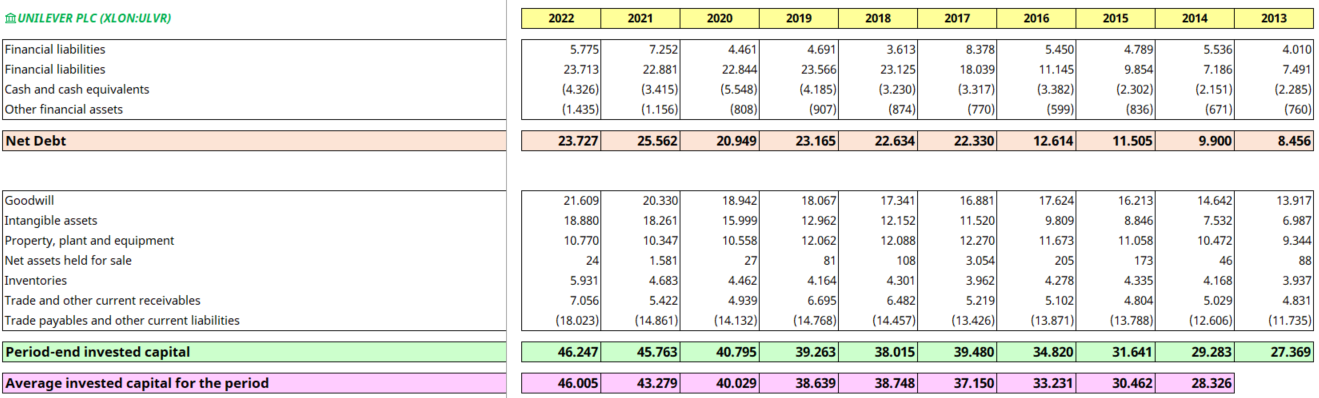

Ya tenemos las cuentas anuales 31/12/2022, por lo que actualizo algunos datos que no tenía:

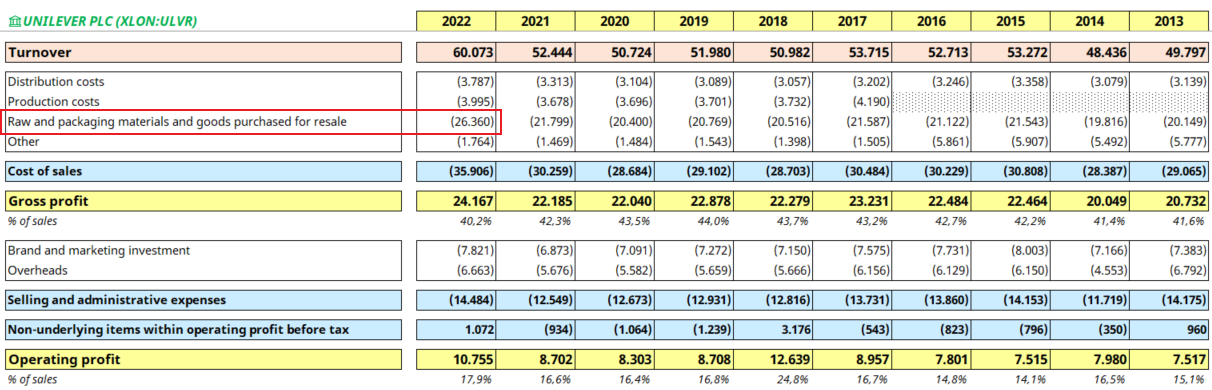

-P&L:

Si se fijan, los dos puntos que ha perdido a nivel de margen bruto se deben a las subidas de las materias primas.

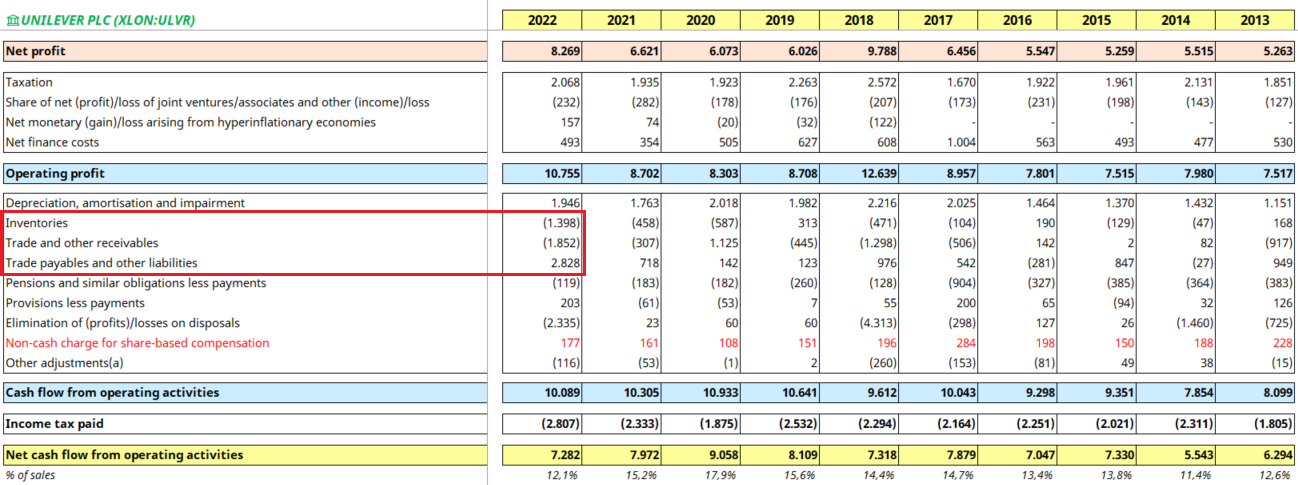

-El working capital como en casi todas drenando cash:

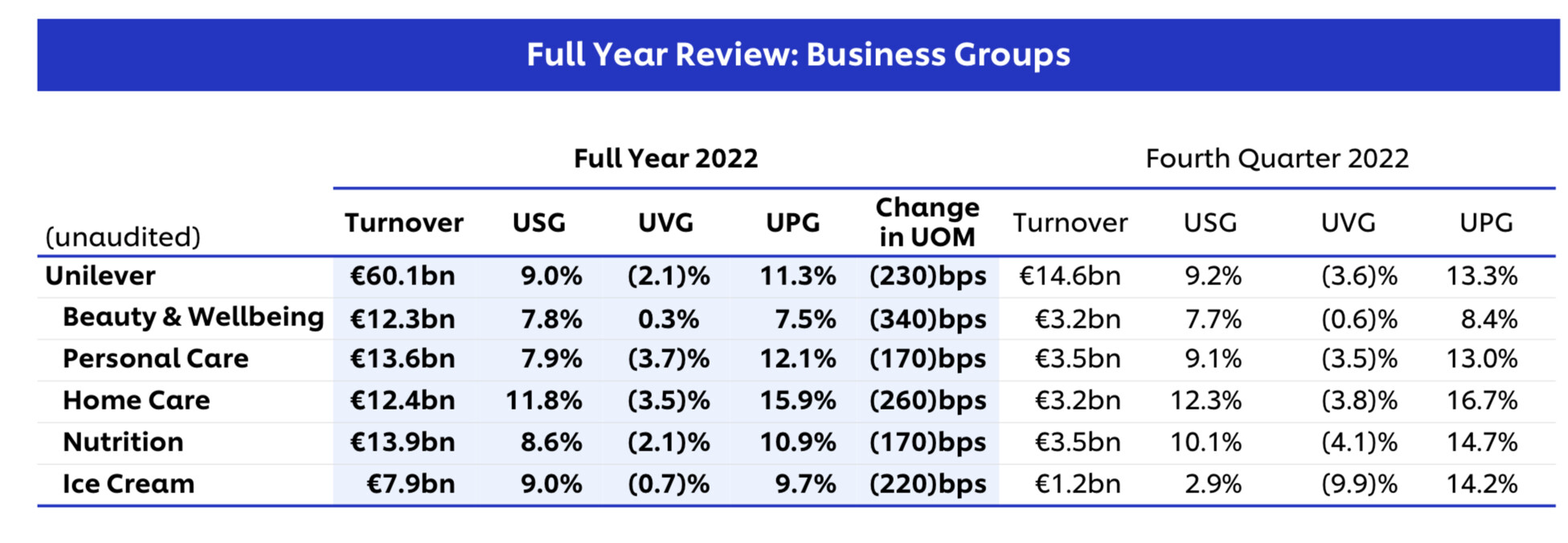

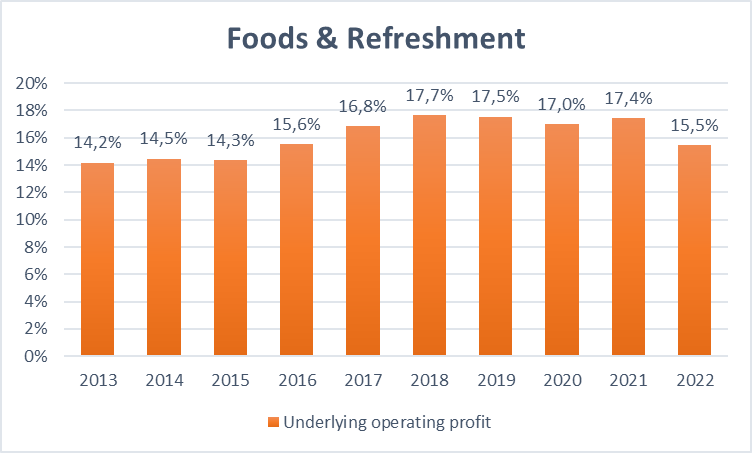

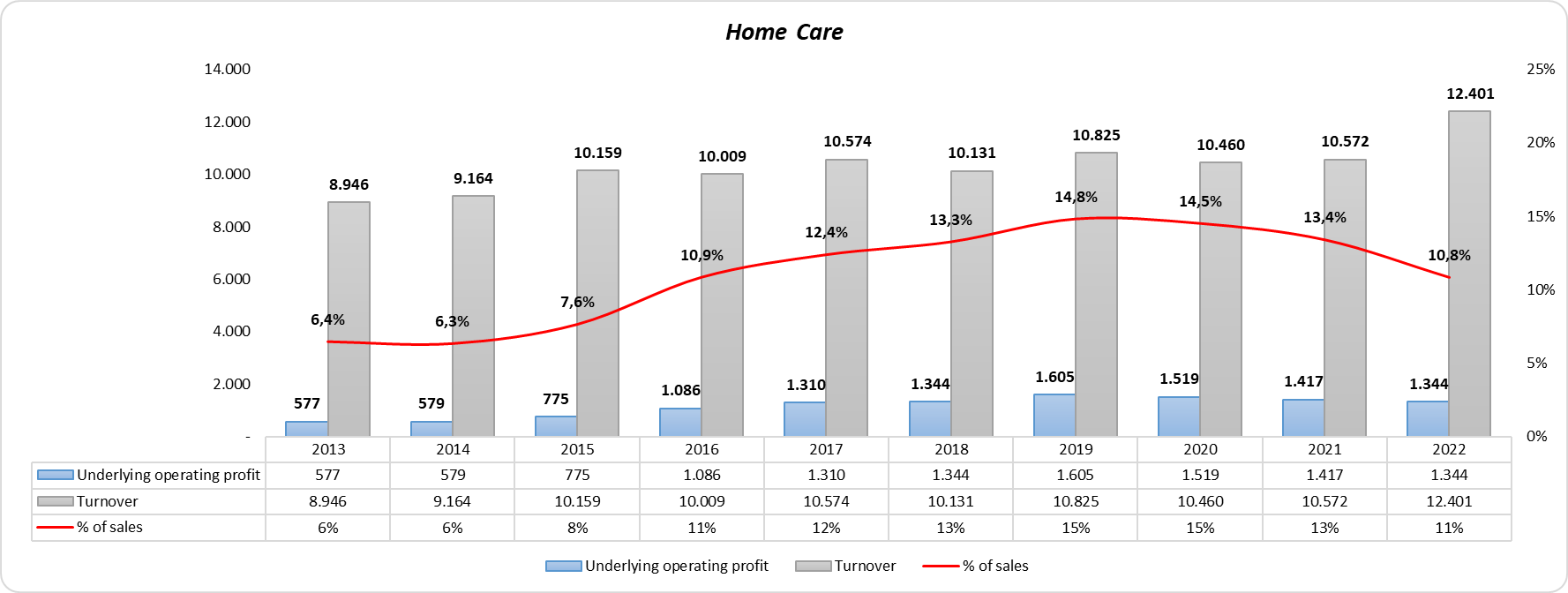

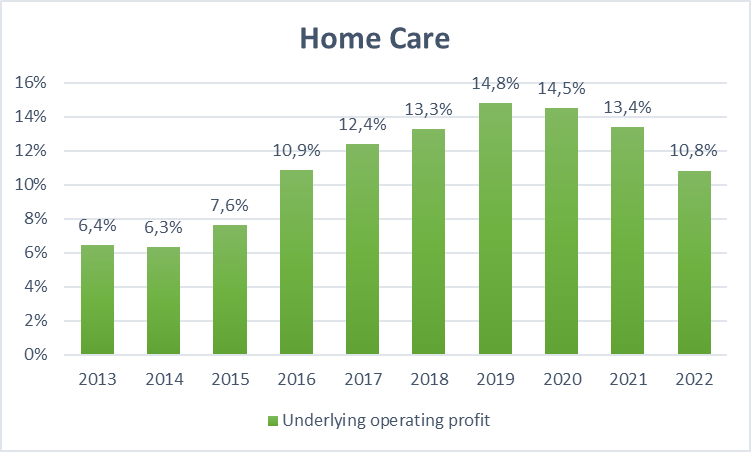

-Divisiones:

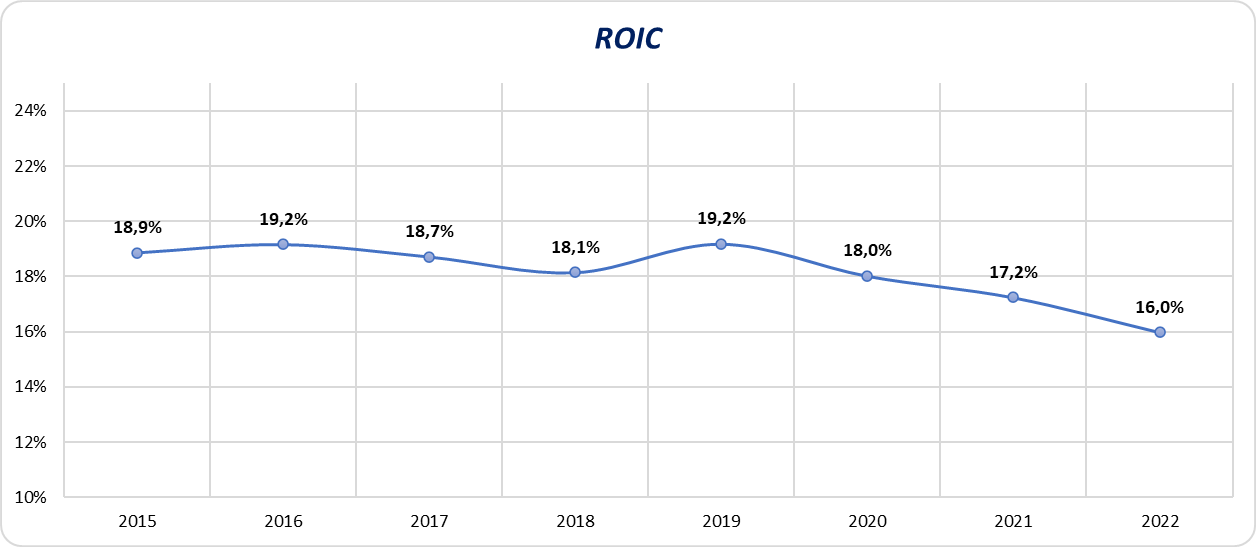

-ROIC:

-FCF:

-EBIT:

-Margen Bruto:

-Deuda neta y capital empleado:

14 Me gusta

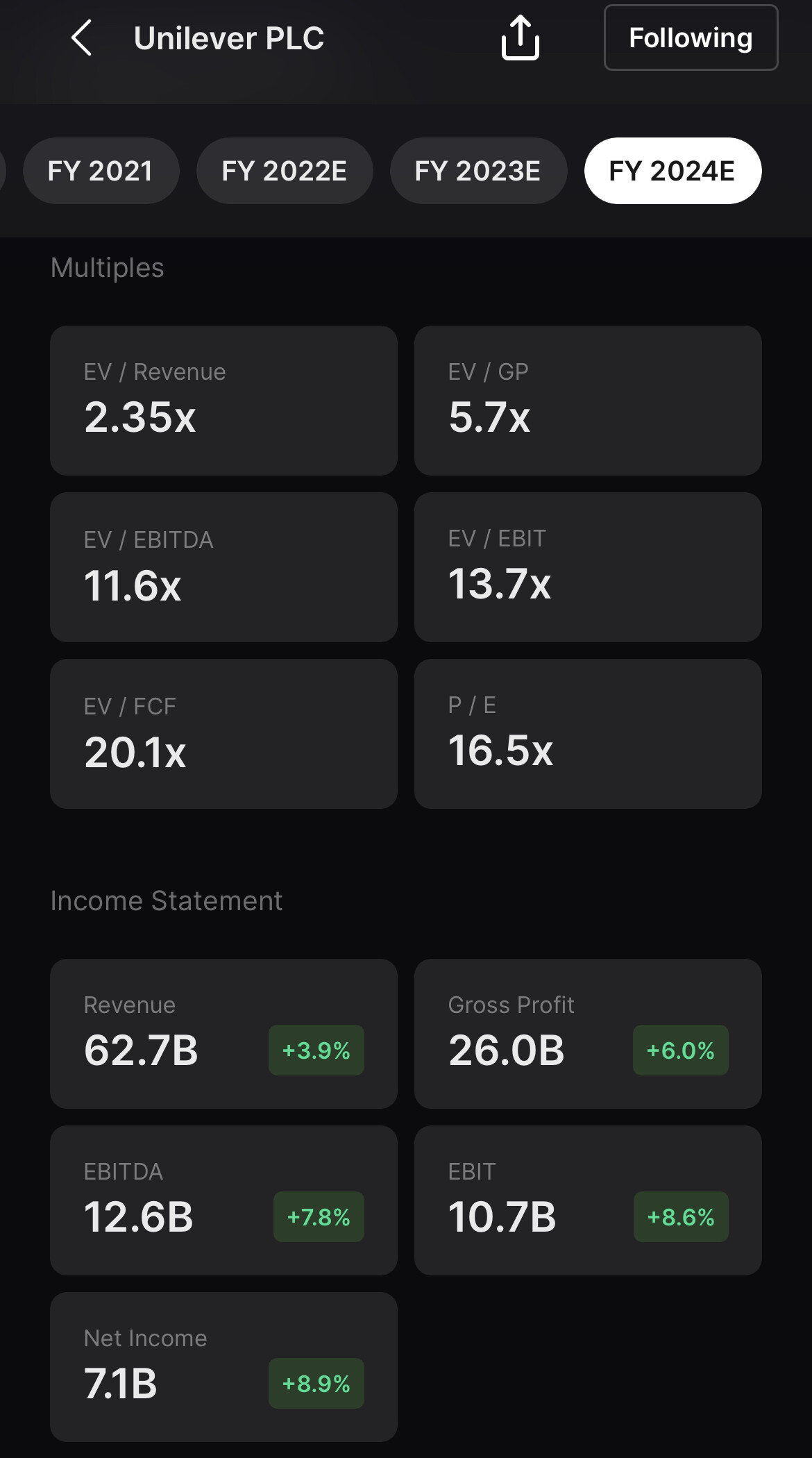

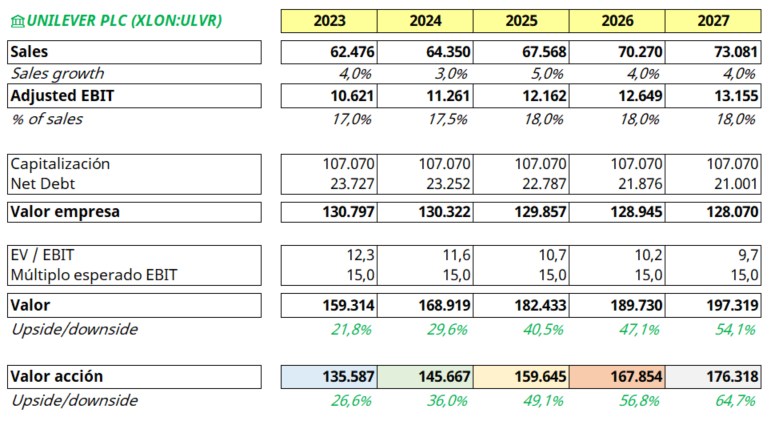

¿Es justo un múltiplo EBIT de 15 veces para Unilever?

Si asumimos una mejora en margen sumado a un crecimiento modesto (3%-4%), ¿cuánto debería de valer?

Sumen a esto el divi

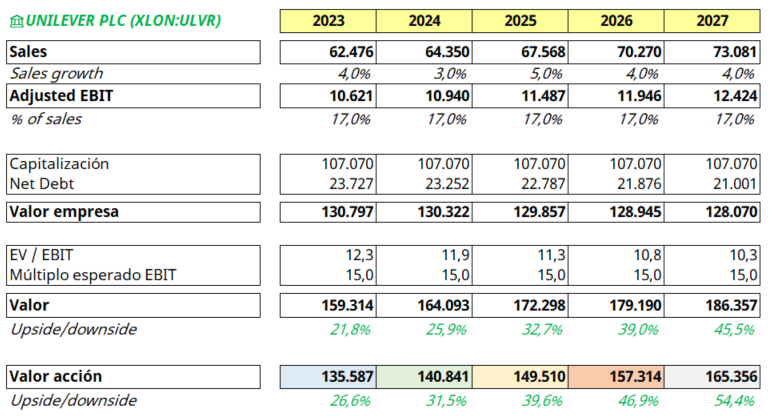

Como siguiente ejercicio, vamos a asumir que el EBIT no consigue llegar al 18%, sino que se queda en el 17%:

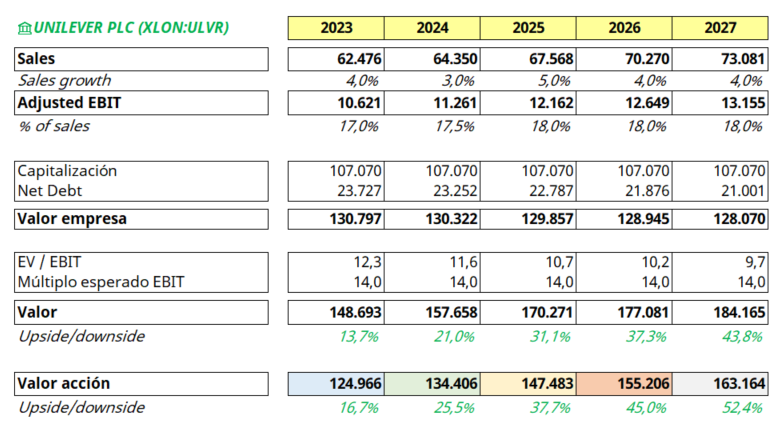

Como otro más, asumamos que el mercado considera que esta empresa, en vez de cotizar a 15 veces EBIT, debería de cotizar a 14:

Lo único que sabemos es que ahora mismo está cotizando a uno de 12,3 veces (sobre el 2023) y no sabemos si seguirá así para siempre.

10 Me gusta

Que parámetros usa como baremo para seleccionar el multiplo al que piensa que debería cotizar? Un histórico largo, los comparables del peer y ajusta o no por moat, múltiplo del sector histórico…

Gracias

1 me gusta