Dividend Kings Performance

Imagine you had $200,000 to invest 25 years ago at the beginning of 1991. Suppose you put half into the S&P 500 Index and invested the other $100,000 equally across each of the current dividend kings that trade on the major stock exchanges (FMCB trades over-the-counter and was excluded for liquidity purposes).

After making your initial investment in each of the dividend kings, you reinvested dividends (ideally through a dividend reinvestment plan) but did nothing else – no rebalancing, no additional capital contributions. You simply bought and forgot.

From 1991 through 2016, your $100,000 in the S&P 500 Index would have compounded at a 9.8% annual rate and grown to just over $1.1 million at the end of 2016. Not bad at all!

But what about your portfolio of dividend kings?

There is some survivorship bias to this study (i.e. it doesn’t account for dividend kings that ultimately lost their crowns), but the dividend kings portfolio grew from $100,000 in 1991 to reach an outstanding value of $2.8 million at the end of 2016, representing a 13.7% annual return.

Dividend Kings Performance

Source: Simply Safe Dividends

Even better, the portfolio of dividend kings had annual volatility of 12.9%, much lower than the S&P 500’s 17.6% volatility during that 26-year period.

Lower volatility means that the value of your dividend kings portfolio would have fluctuated less than the value of your portfolio holding the S&P 500 Index.

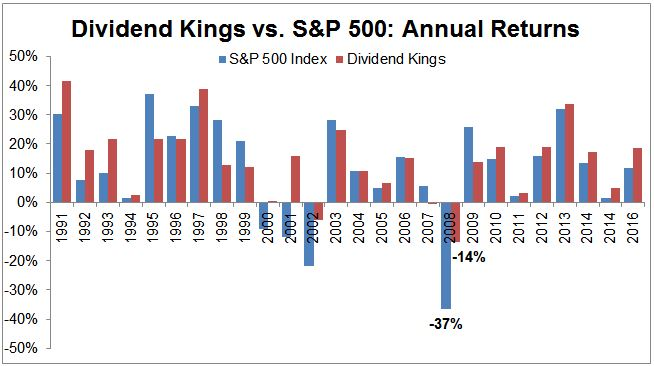

As seen below, the dividend kings significantly outperformed each of the four years that the S&P 500 Index (represented by the blue lines) declined in value. For example, the dividend kings portfolio returned -14% during 2008, easily beating the S&P 500’s total return of -37%. Dividend kings are generally high quality businesses with defensive characteristics that serve them well during bear markets.

Dividend Kings Annual Returns

Source: Simply Safe Dividends

Of course, the performance data above contains a good deal of hindsight bias. After all, who can predict which of the current dividend kings will be able to continue increasing their dividends for the next 25 years?

However, the information does illustrate the correlation between companies that are able to consistently raise their dividends and the value they create for shareholders.

Best Performing Dividend Kings

The best dividend kings from 1991 through 2016 were Lowe’s (LOW), Lancaster (LANC), and SJW Group (SJW). These stocks generated annualized returns of 20.3%, 17.7%, and 15.0%, respectively.

Impressively, each of these dividend kings still maintains a payout ratio less than 50%, leaving plenty of room for them to continue increasing their dividends for years to come.

Worst Performing Dividend Kings

From 1991 through 2016, only one dividend king meaningfully underperformed the S&P 500 – Vectren Corporation (VVC). Vectren is a utility company that primarily provides energy delivery services to natural gas companies located throughout Indiana and Ohio. This dividend king’s stock compounded at an 8.1% annual rate from 1991 through 2016, trailing the S&P 500’s annual return by about 1.7% per year.

All of the other dividend kings compounded faster than the market, although Tootsie Roll (TR) generated a return in line with the market (9.5% per year).

Fastest-Growing Dividend Kings

The fastest growing dividend kings, as measured by annual sales growth over the last five years, are Nordson (NDSN), Cincinnati Financial (CINF), SJW Group (SJW), Lowe’s (LOW), and General Parts (GPC). Their sales have compounded at annual rates of 8.0%, 7.5%, 7.3%, 5.3%, and 4.2%, respectively. After more than 50 years of dividend growth in the bag, these growth rates are remarkable.

Interestingly, only two of these dividend kings are also in the top five when ranked by fastest dividend growth over the last five years. Lowe’s (LOW), Hormel (HRL), Nordson (NDSN), 3M Corporation (MMM), and Parker-Hannifin (PH) have compounded their dividends the fastest at annual rates of 20%, 18%, 17%, 15%, and 12%, respectively.

Aside from 3M Corporation, none of these dividend kings had payout ratios greater than 40% as of 12/31/16, suggesting they have plenty of room for continued dividend growth.

Sector Mix of the Dividend Kings List

Analyzing where each of the dividend kings comes from can be quite insightful. By equal-weighting each of the current 22 dividend kings, we were able to compose the sector mix of the dividend kings list and compare it to the S&P 500.

As seen below, not a single technology stock is to be found in the list of dividend kings. The rapid pace of change and continuous need to invest for growth make consistent dividend payouts less common in this sector. Warren Buffett is notorious for refusing to invest in the technology sector (see his entire dividend portfolio here) because he is uncomfortable forecasting the fast-changing industry’s dynamics several years out.

The consumer staples, industrials, and utilities sectors are weighted much more heavily in the dividend kings list than they are in the S&P 500 Index. These sectors evolve at a much slower pace, providing a more attractive environment for long-term dividend growth.

Dividend Kings Sector Mix

Source: Simply Safe Dividends, Standard & Poors